If you’re thinking about selling your life insurance policy, you’re likely wondering how to get the best deal possible. Fortunately, there are several proven ways to get the most cash for your life insurance, and understanding what affects your offer can help you walk away with a high payout. Whether you’re dealing with a term or permanent policy, this guide outlines what you can do to increase your chances of receiving a strong settlement.

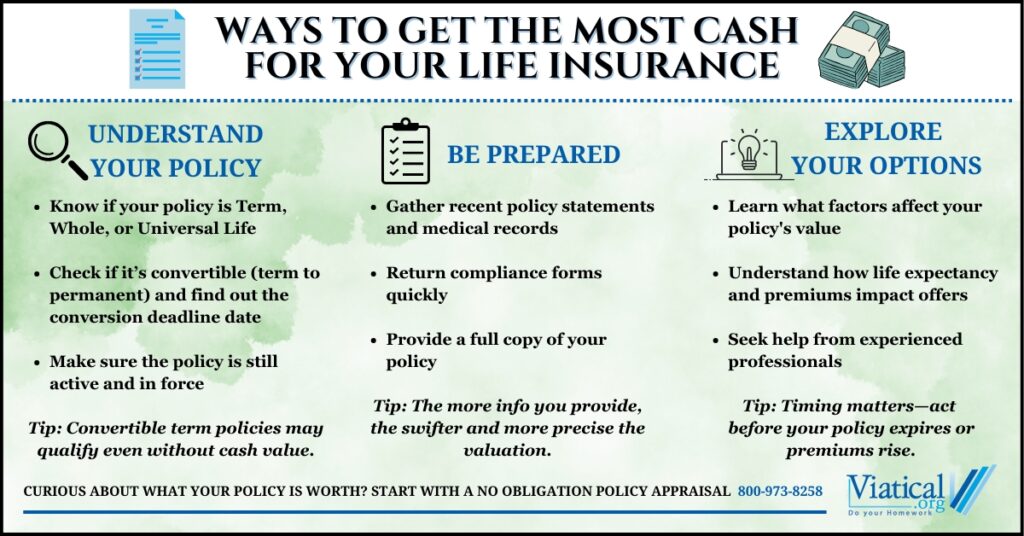

1. Know What Type of Policy You Have

Buyers evaluate life insurance policies differently depending on the type. In general:

- Permanent policies (like whole life or universal life) tend to qualify for higher offers because they don’t expire and often build cash value.

- Convertible term policies may still be eligible for sale—even though they don’t have cash value—especially if they can be converted to permanent coverage without a medical exam.

- Non-convertible term policies can sometimes be sold as annual renewable term, but usually only if the insured has a significant medical condition.

Knowing the details of your policy helps you better understand your market value and ensures you’re comparing offers accurately.

2. Gather All Policy and Medical Documentation

Life settlement companies base their offers on life expectancy estimates and policy details. Having the following ready can speed up the process and improve your offer:

- A complete copy of your insurance policy

- Recent annual statements

- Medical records and medication list

The more accurate and complete your information, the easier it is for buyers to make a competitive offer. Our platform can securely gather needed insurance and medical information, but it is always best to provide everything you have up front as this could possibly reduce the time it takes to gather all necessary information.

3. Learn What Can Affect Your Offer

Several factors influence how much your policy may be worth, including:

- Your age and current health status

- The size of the death benefit

- The cost of annual premiums

- Whether the policy is convertible or permanent

- How many years the policy has been active

Understanding how these elements factor into the valuation process can help you make informed decisions and feel more confident about moving forward.

4. Consider the Timing

Market demand and personal health changes can impact your payout. For example:

- If your health has declined since the policy was issued, your policy may be worth more.

- Market trends—like increased investor interest—can drive up demand and pricing.

- Selling sooner may help you avoid paying ongoing premiums, especially if they’ve become unaffordable.

If you have a convertible policy that is nearing the conversion deadline, now may be the right time to act before that window closes. If possible, it is best to contact us at least 6 months prior to this deadline.

5. Work With Experienced Life Settlement Professionals

Navigating the life settlement process can be complicated, especially when it comes to understanding your rights and evaluating your options. The best professionals can help you:

- Understand the fair market value of your policy

- Explain the steps involved in the process

- Clarify what to expect during the review period

- Provide transparent, no-obligation estimates

At Viatical.org, we help policyholders make informed decisions with confidence. Our resources are designed to educate you on how viatical and life settlements work and guide you through the process.

There are several ways to get the most cash for your life insurance, and it starts with knowing your policy, exploring your options, and making smart decisions based on expert guidance. Whether you’re facing high medical bills, preparing for retirement, or simply want to stop paying premiums on a policy you no longer need, selling your policy could be a valuable option worth exploring.

If you’re ready to see if your policy may qualify, call us today at 800-973-8258