Medicaid Life Settlement

A Medicaid Life Settlement can covert existing life insurance into an insurance account to pay for your care

A Medicaid Life Settlement is the life settlement option that converts existing life insurance into an FDIC insured account used to pay for the cost of assisted living care directly each month. Qualifying for this type of life settlement is quick, and there are no fees or obligations to have your life insurance policy valued. If accepted, you choose the type of assisted living care that is best for you, whether nursing home care, hospice, specialized Alzheimer’s care, or skilled nursing care.

A Medicaid life settlement may change the way you look at your life insurance policy. You may now be eligible to convert your life insurance policy into immediate cash payments to pay for long term care expenses including assisted living, nursing home, hospice and in-home care expenses.

Medicaid Life Settlement:

Every Year, Millions of Seniors Abandon a Life Insurance Policy

…and Get Nothing In Return

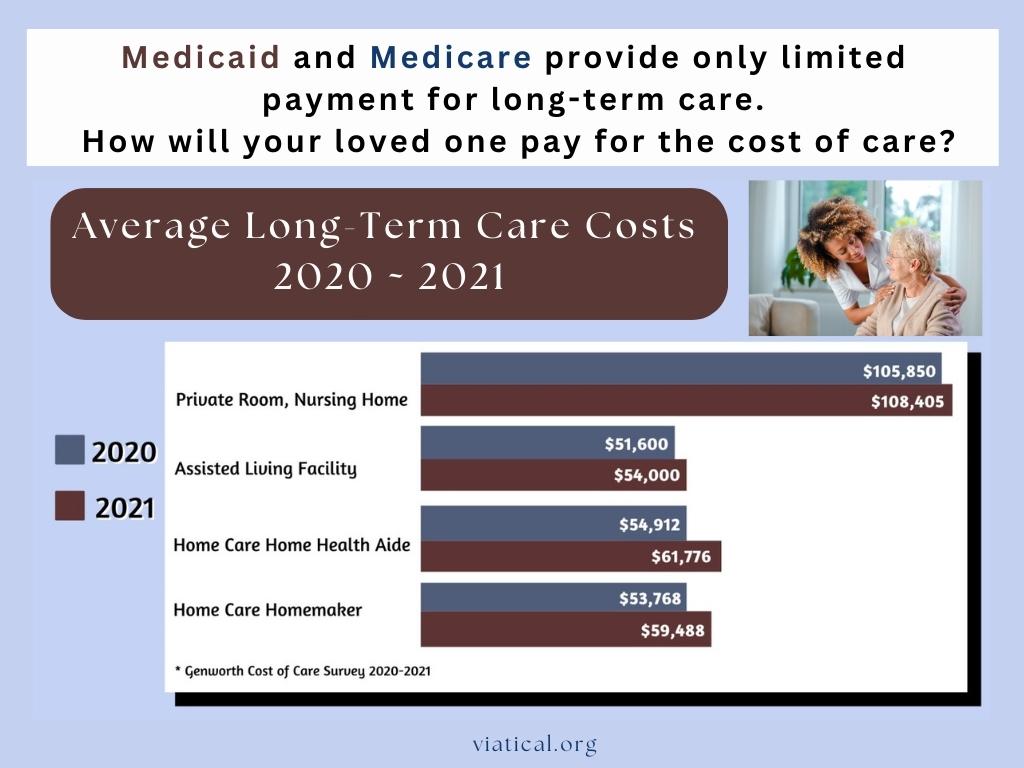

Seniors are throwing away Billions of dollars of cash each year and at the very time they could absolutely use it the most. According to The Life Insurance Settlement Association, more than 80 percent of all life insurance lapses or cancels before it ever pays out in a death benefit. If you are considering using Medicaid to pay for long term care expenses, you should look into the benefits a Medicaid life settlement can provide when deciding how to pay for care.

Too many people cancel their life insurance policies as they qualify for Medicaid to cover their long term care costs. You may feel pressure to liquidate other assets or rely on your family to cover the costs associated with your assisted living. A long term care benefit plan literally takes the insurance policy that you were going to cancel and converts it into payments to the long term care facility of your choice.

Did You Know…

Most life insurance policy can be converted to pay for long term care expenses. If a policy owner no longer needs, or can no longer afford their policy, and is considering letting it lapse or surrendering it for the remaining cash value-then converting it into a Long Term Care Benefit Plan is the answer.

A life insurance policy can pay for long term care expenses.

Before you just cancel your life insurance policy, please take the time to see if it qualifies to be converted into a medicaid life settlement plan. Please also share this message with those you know that may be facing a similar situation. Information and education is the key to making an informed decision.

A life settlement payout refers to the amount of money that a policyholder receives in exchange for their life insurance policy. In a viatical settlement transaction, this typically occurs when an individual with a life-threatening illness sells their life insurance policy to a third-party investor, who will then receive the death benefit once the policyholder passes away.

The amount of the life settlement payout can vary widely, depending on factors such as the policy’s face value, the policyholder’s age and health status, and the prevailing market conditions. Term insurance policies and various other insurance policies may also have different payouts.

To qualify for a life settlement, you typically need to meet certain criteria. First and foremost, you should have a life insurance policy that meets the requirements of potential buyers.

The value of your policy and the potential cash offer will depend on factors such as your age, health and your policy’s terms and premiums. Generally, policies with a face value of $100,000 or more are more attractive in the life settlement market. While there is no specific age limit, individuals over the age of 65 or those with life expectancies of 10 to 15 years may have better chances of qualifying for a life settlement.

It’s important to note that term life insurance policies can also be sold through a life settlement. If you have a term policy and no longer need the coverage, you can explore selling it for cash instead of allowing it to expire.

A life insurance settlement is a transaction in which a policyholder sells their life insurance policy to a third-party investor in exchange for a lump sum payout.

Investors in life settlement funds and senior life settlement investments purchase policies from qualified policyholders. The investor then assumes responsibility for paying the policy’s premiums and collects the death benefit upon the policyholder’s passing.