How Reverse Life Insurance Can Help You

Insurance Companies hate Reverse Life Insurance.

Many large Life Insurance Companies are raising their cost of insurance (COI), but only for their oldest policyholders.[note] Scism, Leslie. “Surprise: Your Life-Insurance Rates Are Going Up.” Wall Street Journal. Wsj.com, 04 Dec. 2015. Web. <http://www.wsj.com/articles/surprise-your-life-insurance-rates-are-going-up-1449225000>

Considering that people are living longer, life insurance rates on the elderly should be going down. Yet Life Insurance Companies are intentionally raising their cost of life insurance so that more and more of our elderly lapse and cancel their policies.

This is being done intentionally and some states have already made significant strides to protect consumers. Please understand that there is often a hidden value in your life insurance if you are over age 65 or chronically ill. Please also understand that Life Insurance Companies would just as soon keep the knowledge hidden and keep your cash altogether.

There are Insurance Companies and security brokerages that will fire agents and advisers for suggesting ‘Reverse Life Insurance’ as an option when you are cancelling your life insurance.

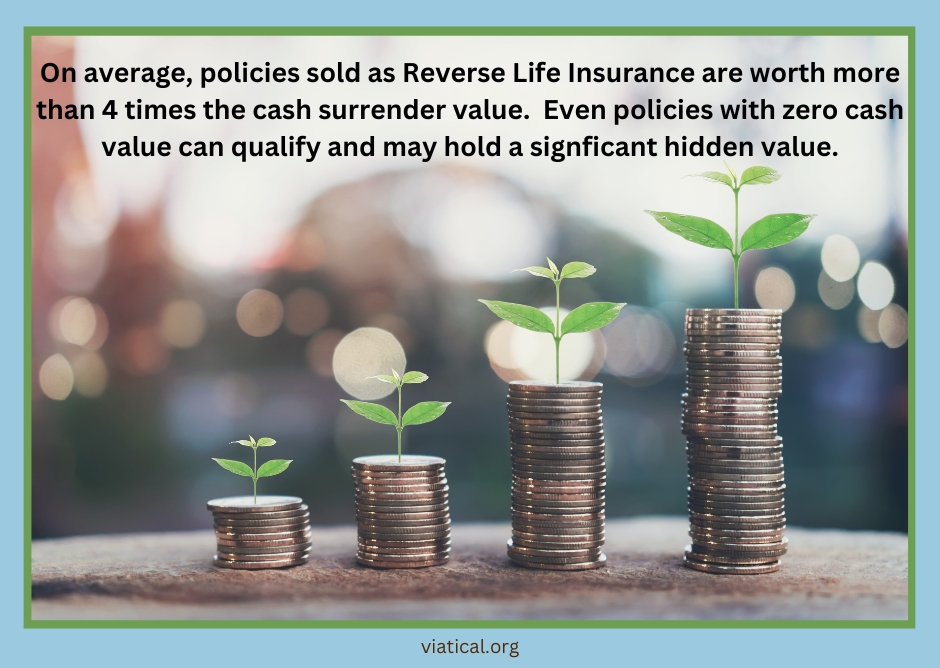

The value in your life insurance policy IS NOT always what the Insurance Company tells you. There is often a significant hidden value that you can access now while you are living. Even some Term Life Insurance policies and Universal Life Insurance policies with zero cash value may have a hidden value that you can access now to cover today’s needs.

Reverse Life Insurance is simply selling some or all of your life insurance policy for cash. On average you can get 4 to 8 times more than what your Insurance Company will give you. If you are selling your convertible term life insurance policy or an insurance policy that has no cash value, your insurance company is essentially offering zero for your policy.

The cash value of your life insurance policy is what your Insurance Company will give you if you cancel or surrender. The cash value is just their take it or leave it offer when taking back your policy, but life insurance is an asset. You should always have more than one bid when selling an asset, which is essentially what you are doing.

88% of life insurance contracts lapse for lack of payment or are cancelled without ever paying a death claim. “Business Economics and Public Policy.” Wharton. University of Pennsylvania. Web. <https://bepp.wharton.upenn.edu/>

Insurance Companies factor a high lapse factor into their profit margins and now they are doing nothing short of trying to force senior citizens to lapse their life insurance. It is wrong that you can pay into your insurance policy for 20 years and then your Insurance Company simply changes the rules so that you can no longer afford your policy.

You purchased your life insurance to protect your family or a business. As you age, often your needs change from replacing your earnings in the event of your death to your own immediate long term care issues. If you are already struggling to pay insurance premiums, your cash value is going down and you really no longer need the life insurance; the decision to cancel your life insurance policy is an easy one for most people.

So why would your life insurance agent or your financial adviser let you cancel your life insurance policy and forfeit the hidden value that may be in your life insurance policy? The answer is either ignorance or fear. There is only about 60% awareness of the secondary market for life insurance amongst financial advisers, so he/she may not know. “Life Settlement Research,” Wealth Management. The Lifeline Program. Dec. 2014. Web. <http://www.thelifeline.com/sites/default/files/FINAL_LifeSettlements-WP_Wealthmgmt_2.6_15.pdf> It is often the case that your adviser knows that you can possibly sell your life insurance policy for cash but is not allowed to tell you. There is something inherently wrong with an ‘Adviser’ not advising.

There are actually insurance agents and ‘Advisers’ that are strictly forbidden from mentioning Reverse Life Insurance as an alternative, even if you need the money for long term care expenses.[note]Bayston, Darwin, and Michael Kreiter. “Why Agents Can’t Mention Life Settlements.” LifeHealthPro: Life & Health Insurance News & Sales Tips. LifeHealthPro, 19 Sept. 2014. Web. <http://www.lifehealthpro.com/2014/09/19/why-agents-cant-mention-life-settlements> Now that the word about Reverse Life Insurance is spreading, states are passing laws to protect America’s seniors from this ageist targeting.

States Passing Laws to Protect Seniors’ Right to Reverse Life Insurance

Georgia now legally protects insurance agents from unfair termination. “Georgia Code: Title 33 — Insurance.” Justia Law. N.p., 2006. Web. 12 Nov. 2016. <http://law.justia.com/codes/georgia/2006/33/33.html>. That is correct, agents can be terminated for merely telling you the truth about the hidden value in life your insurance.

Oregon law now states that Insurance Companies must inform their clients that there is a Reverse Life Insurance option available. Disclosure by Insurance Company to Policy Owner. 744th Chapter. Vol. 15. N.p.: ORS, 2015. Oregon Laws. Web. <http://www.oregonlaws.org/ors/744.362> This previously hidden information is changing the quality of lives.

The Supreme Court already supports your right to sell or convert your unneeded or unaffordable life insurance policy to cash. Texas felt consumer awareness was so low that they passed Medicaid Life Settlement legislation in 2014 publicly supporting your right to sell your life insurance policy.[note]”Life Insurance and Medicaid Long-term Services and Supports.” How to Get Help. Texas Health and Human Services Commission, n.d. Web. 12 Nov. 2016. <https://yourtexasbenefits.hhsc.texas.gov/programs/health/disability-or-65plus/life-insurance-and-medicaid>.

Texas was the first state to pass legislation approving the spending of public funds to promote Medicaid Life Settlements. A Medicaid Life Settlement is just one of the many Life Settlement options available if you qualify to sell your life insurance policy. The cash you can get from selling your life insurance policy can be significant to the point of keeping you off of state medicaid rosters. You maintain control of the quality of your life, versus spending down your assets and becoming a ward of your state.

It is estimated that our elderly unknowingly lapse over 100 billion dollars of life insurance each year. Bayston, Darwin. “$112 Billion in Life Insurance Policy Lapses by Seniors – Shame on All of Us!” LifeHealthPro: Life & Health Insurance News & Sales Tips. ALM Media LLC, 12 Mar. 2015. Web. <http://www.lifehealthpro.com/2015/03/12/112-billion-in-life-insurance-policy-lapses-by-sen> A reduction in income or an increase in expenses and insurance premiums can drain your bank account and destroy your peace of mind.

If you are over the age of 65 and your health has slipped, you may have a hidden value inside of your life insurance policy. Reverse Life Insurance enables you to receive this value as a lump sum of cash now, when you need it.

Reverse Life Insurance is a way to sell some or a portion of your life insurance policy for cash. Not everyone qualifies for Reverse Life Insurance. Qualification does depend on varying factors including: age, health status, and policy type. Talking with one of our representatives will help clarify your options.

Reverse Life Insurance pays you to live.

Reverse life insurance, also known as a life settlement, is a financial transaction in which a policyholder sells their life insurance policy to a third-party buyer, who then becomes the new beneficiary of the policy. This transaction can be a great option for those who no longer need their life insurance coverage and could benefit from the financial payout.

Whether you have a term policy or a permanent life insurance policy, you may be able to sell it for a lump sum payment through a life insurance settlement. By doing so, you could receive a lump sum cash payout that you can use for any purpose you choose.

While you cannot reverse a life insurance policy, you can sell it through a life settlement agreement. Life settlements are becoming an increasingly popular option in the life insurance market, as more and more people are looking for ways to benefit from their policies.

Those who qualify for a life settlement typically include policyholders who are 65 or older and have a life insurance policy with a face value of at least $100,000. However, even those who do not meet these criteria may still have life settlement options available to them.

While most life insurance policies do not provide a payout until after the policyholder’s death, there is one option that can give you money back while you’re still alive: a life settlement.

A life settlement is a financial transaction in which a policyholder sells their life insurance policy to a third-party buyer for a lump sum payment. This can be a great option if you no longer need your policy and are in need of funds.

Most types of life insurance policies can qualify, even convertible term policies and universal life policies with no cash surrender value.