The latest 2025 life settlement market data released by the Life Insurance Settlement Association (LISA) highlights a reality many policyowners still do not realize: surrendering a life insurance policy may not provide the highest available value.

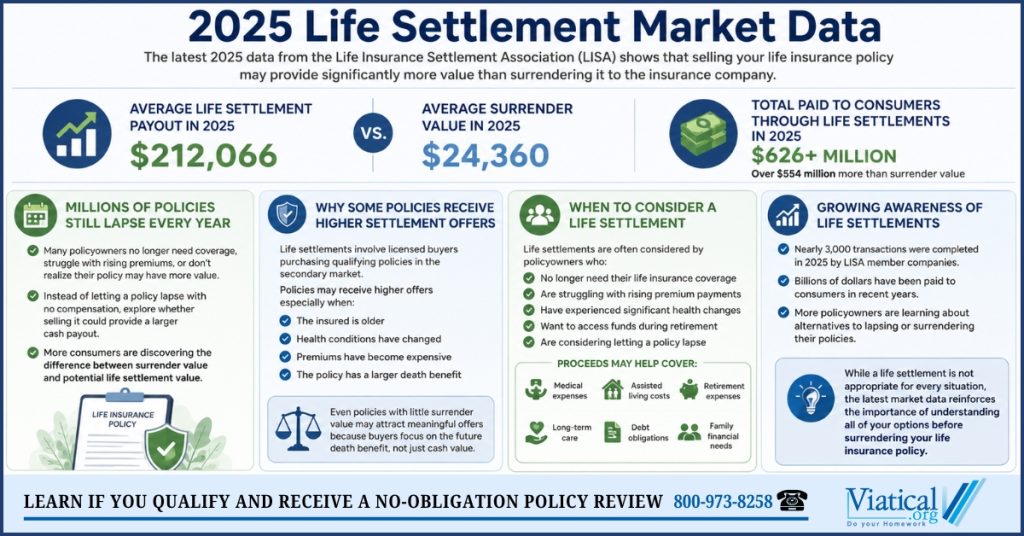

According to the newly released report, the average life settlement payout in 2025 was $212,066, compared to an average surrender value of just $24,360. Qualifying policyowners who sold their policies received substantially more than the amount offered directly by the insurance company.

The report also shows that consumers received more than $626 million through life settlement transactions during the year, representing over $554 million more than surrender value.

Millions of Policies Still Lapse Every Year

Despite growing awareness of life settlements, millions of life insurance policies continue to lapse or surrender annually in the United States.

In many cases, policyowners may no longer need coverage, may be struggling with rising premiums, or may simply be unaware that their policy could have value beyond the surrender amount offered by the insurance company.

Rather than allowing a policy to lapse with no compensation, some seniors and individuals with serious health conditions choose to explore whether selling the policy may provide a larger cash payout.

The latest market data suggests that more consumers are beginning to understand the difference between surrender value and potential life settlement value.

Industry experts have pointed out for years that many consumers mistakenly assume surrendering a policy back to the insurance company is their only option. However, the continued growth of the secondary market shows that more policyowners are learning about alternatives that may provide additional financial value.

Why Some Policies Receive Higher Settlement Offers

Cash surrender value is determined by the insurance company based on the policy’s accumulated value and contract terms.

A life settlement, however, involves licensed buyers purchasing qualifying life insurance policies in the secondary market.

Because of this, policies that may appear to have limited surrender value can sometimes receive substantially higher settlement offers, particularly when:

- The insured is older

- Health conditions have changed

- Premiums have become expensive

- The policy has a larger death benefit

Not every policy qualifies for a life settlement, but the 2025 data demonstrates how significant the difference may be for qualifying policyowners.

In some situations, policies with very little surrender value may still attract meaningful settlement offers because investors are evaluating the future death benefit rather than simply the accumulated cash value within the policy.

When to Consider a Life Settlement

Life settlements are often considered by policyowners who:

- No longer need their life insurance coverage

- Are struggling with rising premium payments

- Have experienced significant health changes

- Want to access funds during retirement

- Are considering letting a policy lapse

In general, larger policies and policies owned by older individuals or people with serious health conditions tend to attract more interest from buyers in the secondary market.

Some policyowners use proceeds from a life settlement to help cover:

- Medical expenses

- Assisted living costs

- Retirement expenses

- Long-term care

- Debt obligations

- Family financial needs

For some, a life settlement may provide financial flexibility at a time when maintaining an unwanted or unaffordable policy no longer makes sense.

Others may simply decide they would rather access a portion of the policy’s value while they are still alive instead of continuing to make premium payments on coverage they no longer intend to keep.

Growing Awareness of Life Settlements

The 2025 LISA report also reflects continued growth within the life settlement industry itself. Nearly 3,000 transactions were completed during the year by LISA member companies, and the report noted billions of dollars paid to consumers over recent years.

As more policyowners research alternatives to lapsing or surrendering their policies, awareness surrounding life settlements continues to grow.

While a life settlement is not appropriate for every situation, the latest market data reinforces the importance of understanding all of your options before surrendering your life insurance policy.

To learn if your policy may have a hidden value that far exceeds the cash surrender value, please give us a call today. 800-973-8258