When a term life policy is nearing the end of its level premium period, many people assume their coverage is about to become worthless. In reality, it is important to check your term policy’s conversion options before it expires, because buyers in the life settlement and viatical settlement market often require a policy to be convertible. Knowing whether that feature exists can determine if your policy is worth evaluating for a potential sale.

Why Conversion Options Matter to Buyers

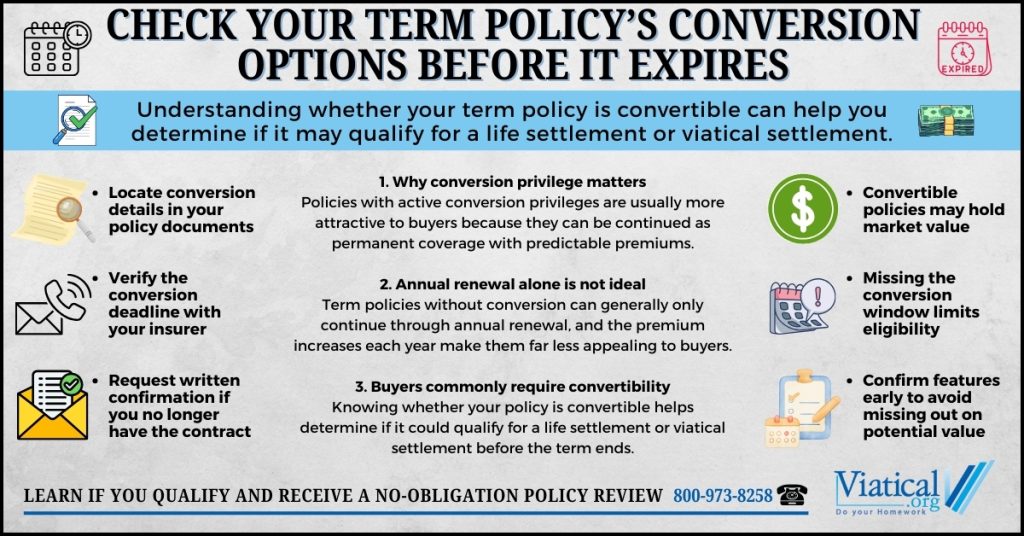

Most term policies technically offer two ways to continue coverage after the initial term ends:

- Renewal as annual renewable term

- Conversion to a permanent policy, if the contract allows it

Annual renewable term keeps coverage in force, but the premiums usually increase sharply each year. Those rising costs make it difficult for individuals to afford and unattractive for potential buyers who prefer predictable long-term premium obligations.

A conversion option is different. It allows the policy to be changed into a permanent form of coverage with guaranteed benefits and a more predictable premium structure, without requiring a new medical exam. Buyers strongly prefer policies that are convertible because they can decide whether to exercise that right. The presence of a conversion privilege often makes the difference between a policy being marketable or not.

By contrast, most non-convertible term policies can only continue through annual renewal, and the rapidly increasing premiums mean these policies are rarely considered good candidates for life settlements. In some cases, they may still qualify if the insured has a significant health concern, so it is always best to check your eligibility.

Confirming Whether Your Policy Has a Conversion Option

The goal is not to convert the policy yourself. The goal is to understand whether the conversion option exists so you know if a buyer might be interested. It is important to be aware of term conversion deadlines and life settlements options.

You can usually find conversion details here:

- The policy schedule or specification pages

- A section labeled “conversion privilege” or “conversion option”

- Any riders that modify or extend conversion rights

- The pages discussing term length, renewability, and premium structure

If you do not have the original contract, you can contact your insurance company and ask:

- Is this policy currently convertible?

- Up to what date or age can it be converted?

- Are there any limitations on what it type of policy it can be converted to?

Ask the insurer to send written confirmation of this information. You are only gathering facts about the policy. This does not obligate you to make changes.

What the Conversion Deadline Means for Settlement Eligibility

Every convertible term policy has a conversion deadline, usually tied to a specific age or the end of the level term period. Once that date passes, the conversion privilege is gone.

If the conversion window is still open and the insured’s health has declined since the policy was issued, the policy may be more attractive in the secondary market. Buyers take comfort in knowing they can convert the policy to permanent coverage in the future if it suits their pricing and risk models. Policies that are no longer convertible, or were never convertible, generally face more limited interest.

Understanding the Value Before the Policy Ends

Before your term coverage reaches the end of its level period, take time to identify whether a conversion privilege is built into the contract and whether it is still available. Buyers in the life settlement and viatical settlement market often look specifically for convertible term policies, and that single feature can determine whether your expiring term policy has a hidden value.

To learn if you qualify and to obtain a no-obligation policy appraisal, please give us a call at 800-973-8258.