Managing a long-term health condition often brings ongoing costs that can feel overwhelming. Financing chronic illness involves more than simply paying medical bills, it’s about creating a sustainable plan to cover treatments, medications, supportive care, and everyday living expenses while maintaining as much stability and quality of life as possible. Understanding the available financial tools can help patients and their families make informed decisions.

Understanding the Costs

Chronic illnesses such as heart disease, COPD, diabetes, autoimmune diseases, and progressive neurological disorders often require:

- Frequent doctor visits and specialist consultations

- Prescription medications, sometimes including high-cost biologics or specialty drugs

- Hospital stays, surgeries, or outpatient procedures

- Home health care or rehabilitation services

- Medical equipment such as oxygen tanks, wheelchairs, or monitoring devices

- Transportation to and from appointments

- Adjustments to the home for accessibility

- Reduced work hours or early retirement, leading to lost income

These expenses can persist for years, making careful financial planning essential.

Health Insurance Coverage and Gaps

Health insurance is a starting point for many, but it rarely covers every expense. Patients may face:

- High deductibles and copays

- Coinsurance for costly treatments

- Limited coverage for certain therapies or out-of-network providers

- Caps on physical therapy, occupational therapy, or home health care visits

- Exclusions for experimental or alternative treatments

Reviewing your policy carefully and speaking with your insurer about prior authorizations and appeals can help minimize out-of-pocket costs.

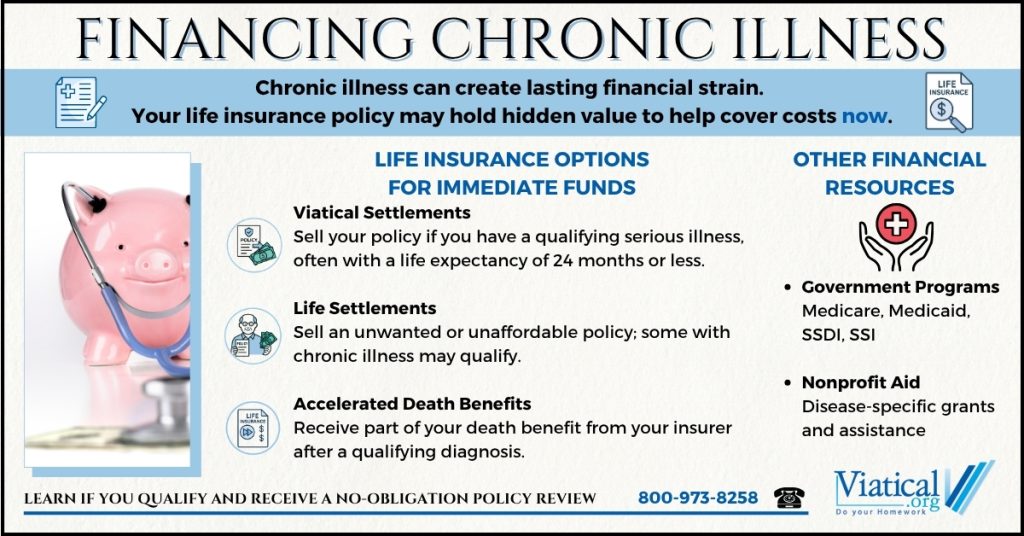

Government and Nonprofit Assistance

Several programs can help bridge coverage gaps:

- Medicare and Medicaid – Available based on age, disability status, or income level.

- Social Security Disability Insurance (SSDI) – Provides monthly income to those unable to work due to a qualifying disability.

- Supplemental Security Income (SSI) – Offers additional support for individuals with limited income and resources.

- State and local health programs – May offer prescription assistance, transportation services, or subsidized care.

- Disease-specific foundations – Organizations for conditions like multiple sclerosis, cystic fibrosis, or cancer often offer grants or patient assistance programs.

Life Insurance as a Financial Resource

For those with an existing life insurance policy, the policy itself can sometimes be used to generate immediate funds. Three common options are:

Viatical settlements

This option allows a policyholder with a qualifying serious illness to sell their life insurance policy for a lump-sum payment. Viatical settlements are typically available to individuals with a life expectancy of 24 months or less. The payment is always higher than the policy’s cash surrender value and can be used for medical bills, in-home care, or any personal expenses. Because the funds come from the sale of the policy, there are generally no restrictions on how they can be spent.

Life settlements

Similar to viatical settlements, life settlements are available to individuals who may not be terminally ill but still wish to sell an unwanted or unaffordable policy. They are most often used by seniors over the age of 65, but some younger people with chronic illnesses may also qualify. The payout is determined by factors such as age, health status, and the policy’s terms. Life settlements can be especially useful if a policy is no longer needed for its original purpose, such as providing for dependents.

Accelerated death benefits

This option allows a policyholder to receive a portion of their death benefit directly from the insurance company, typically after a diagnosis of a terminal illness or certain chronic conditions. The remaining death benefit is then paid to beneficiaries upon the policyholder’s passing. While this is a valuable resource for those who meet the requirements, not all policies include an accelerated death benefit or living benefit rider. Please consult with your insurance company regarding the specifics of your policy and to find out how to get an accelerated death benefit.

Each of these options has different eligibility requirements, tax implications, and impacts on beneficiaries. For many living with a chronic illness, reviewing these possibilities can uncover a source of funding that helps cover care costs, reduce financial stress, and provide flexibility during a difficult time.

Learn More About Your Options

The financial challenges of chronic illness are often as persistent as the medical ones. While health insurance, public programs, and nonprofit aid can help, exploring options within an existing life insurance policy can open the door to meaningful financial relief for financing long term chronic illness. Whether through a viatical settlement, life settlement, or accelerated death benefit, these options can provide access to funds that help maintain quality of life, support treatment, and ease the burden on loved ones.

To learn if you qualify and which option may be best for your unique situation, please give us a call at 800-973-8258. We have been helping patients access the hidden value in life insurance for nearly 20 years.