When cancer comes back, the emotional and financial toll can be overwhelming. For many patients, the return of a previous cancer, known as a recurrence or relapse, means more aggressive treatment, extended time away from work, and higher out-of-pocket costs. Learning how a viatical settlement can help when cancer comes back can open the door to financial relief during one of life’s most challenging moments, allowing patients to focus on care instead of costs.

A viatical settlement allows someone with a serious or terminal diagnosis to sell their life insurance policy to a third party for a lump sum of cash. The payout is higher than the policy’s cash surrender value, but less than the death benefit. The funds can offer financial support for cancer treatment and can be used however the policyholder chooses. They can help with covering treatment costs, paying down debt, traveling to see family, or simply improving quality of life.

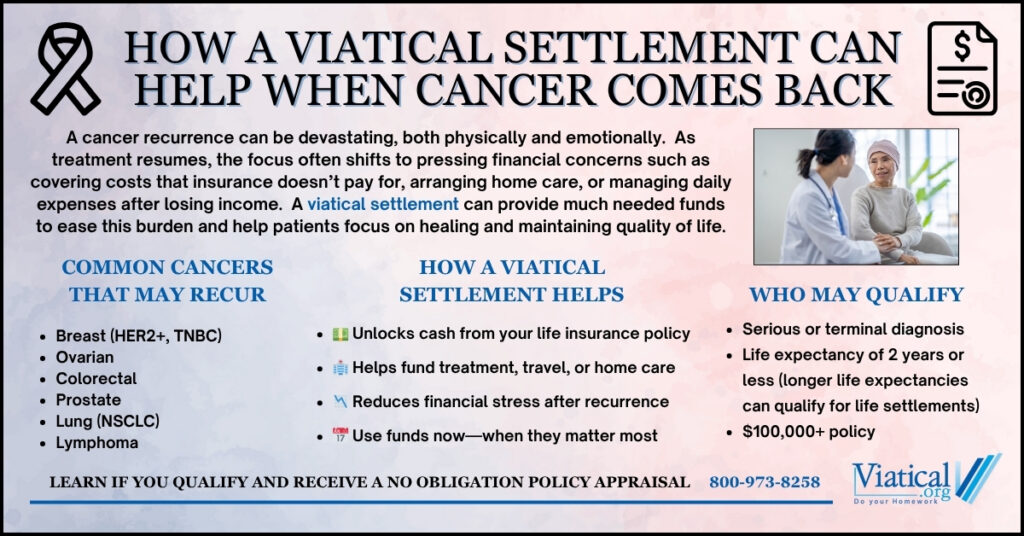

Types of Cancer Where Recurrence is Common

Some of the most commonly recurring cancers include:

- Breast cancer, especially triple-negative or HER2-positive types. Hormone receptor-positive cancers can also recur years later.

- Ovarian cancer, where recurrence within a few years is common despite initial treatment success.

- Colorectal cancer, particularly stage III cases or those with lymph node involvement.

- Prostate cancer, where PSA levels can rise again, often signaling a biochemical recurrence.

- Non-small cell lung cancer (NSCLC), which may return locally or spread to other organs.

- Lymphomas, including Hodgkin lymphoma and diffuse large B-cell lymphoma, which can relapse after remission.

When these cancers return, the next phase of treatment can vary depending on the cancer type, stage, and location. Common options include radiation therapy, chemotherapy, targeted therapies like trastuzumab (Herceptin) or bevacizumab (Avastin), and newer immunotherapies such as pembrolizumab (Keytruda) and nivolumab (Opdivo). In some cases, patients may explore clinical trials or travel to specialty centers, which can further increase expenses.

Financial Pressure After a Cancer Recurrence

Cancer recurrence often brings with it a more complex and expensive treatment plan. While using insurance may cover some costs, copays, coinsurance, out-of-network providers, and uncovered treatments can quickly become unmanageable. Many patients also experience reduced or lost income from time away from work.

That’s where a viatical settlement can make a real difference. If you own a life insurance policy and have received a diagnosis indicating a limited life expectancy, you may be eligible to sell that policy for immediate cash. This can offer peace of mind and flexibility to make decisions based on your health needs, not your financial constraints.

Who Qualifies for a Viatical Settlement?

You may qualify for viatical settlements if:

- You have a life-threatening diagnosis, often with a life expectancy of two years or less

- Your life insurance policy is generally at least two years old

- The policy has a face value of $100,000 or more

- You are the owner and can transfer ownership and beneficiary rights

Even if you didn’t qualify when you were first diagnosed, a recurrence may change that, particularly if the prognosis has worsened.

A Real Option During a Difficult Time

Thousands of cancer patients have used viatical settlements to access care they wouldn’t otherwise afford, reduce financial stress, or simply live more comfortably. Whether you need to pay for travel to a treatment center, afford a drug not covered by insurance, or spend more time with family, this option can provide critical financial freedom.

Understanding how a viatical settlement can help when cancer comes back can give patients a practical way to ease financial burdens and make more empowered choices during a difficult time.

If you or a loved one is facing a cancer recurrence and owns a life insurance policy, exploring a viatical settlement could be a meaningful next step. To learn if you qualify, please give us a call at 800-973-8258