If you are wondering how much do life settlement companies pay, the answer depends on several key factors including your age, health condition, policy type, and the size of your death benefit. In general, a life settlement pays more than the cash surrender value but less than the full death benefit. For many policyholders facing serious illness or financial strain, it can provide access to funds that would otherwise remain unavailable.

What Determines the Payout Amount

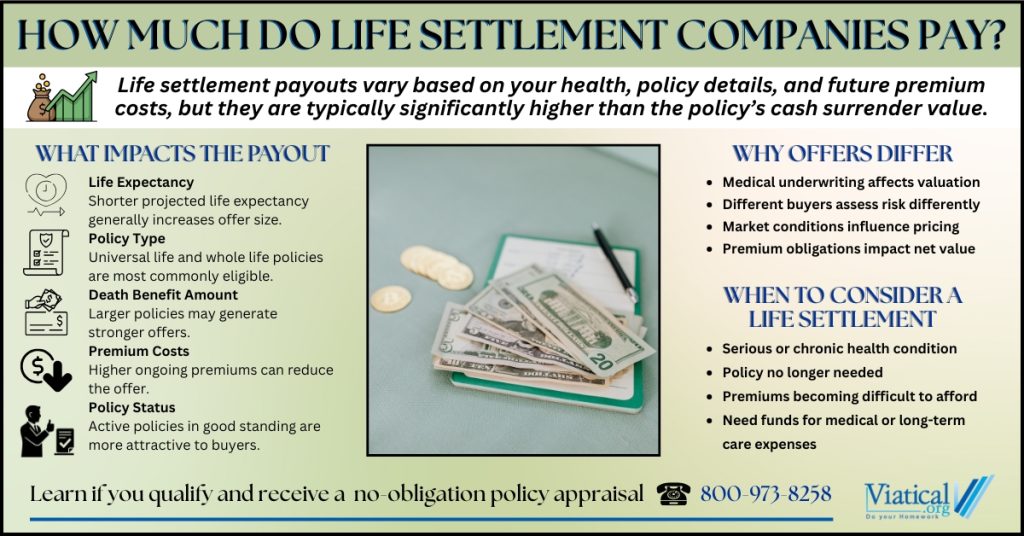

Life settlement companies evaluate policies based on risk and projected return. The most important factors influencing life settlement payout range include:

Life Expectancy

Buyers review medical records to estimate life expectancy. A shorter life expectancy generally results in a higher offer because the buyer expects to collect the death benefit sooner.

Policy Type

Permanent policies such as universal life and whole life are more commonly eligible. Some term policies may qualify, especially if they are convertible.

Death Benefit Size

Larger policies typically attract stronger offers because the potential return is higher. $100,000 is typically the minimum face value that will qualify.

Premium Costs

The buyer becomes responsible for future premiums. If premiums are high, the offer may be lower because ongoing costs reduce the investment value.

Policy Status

Policies that are in force and current on premiums are more attractive. Lapsed or near-lapse policies may still qualify in some cases but require additional review.

Typical Life Settlement Payout Ranges

While every case is different, most life settlements fall within a predictable range:

- 10 percent to 25 percent of the death benefit is common

- In some advanced illness cases, offers may be as high as 80% of the face value

- Offers are usually several times greater than the surrender value

For example, a $250,000 policy might generate an offer between $25,000 and $60,000 depending on the insured’s health profile and policy structure.

It is important to understand that life settlement companies do not simply offer a flat percentage. The valuation process involves medical underwriting and financial modeling. Every case is truly unique and requires a policy appraisal.

Why Payouts Vary So Much

Two people with the same policy amount can receive very different offers. Health status plays a major role. A policyholder with a serious or progressive condition may receive a stronger offer than someone with stable chronic issues.

Market conditions can also influence payouts. Investor demand, interest rates, and life expectancy modeling trends affect pricing.

This is why comparing offers can be important. Different buyers may evaluate the same policy differently.

How Life Settlements Compare to Other Options

Before accepting a surrender offer from your insurance company, it is worth exploring whether selling the policy could generate more value.

A surrender value is determined by the insurance carrier and often represents a small portion of the total death benefit. A life settlement, by contrast, is negotiated in the secondary market.

Other alternatives may include:

- Accelerated death benefits

- Policy loans

Each option has different eligibility requirements and financial implications.

Who Should Consider a Life Settlement

Life settlements are most commonly pursued by:

- Individuals with serious or chronic health conditions

- Policyholders who no longer need or want coverage

- People struggling with medical bills or long-term care expenses

- Families seeking liquidity during financial hardship

If maintaining premiums has become difficult or the original purpose of the policy no longer applies, selling may be worth exploring.

Getting an Accurate Estimate

The only way to determine what your specific policy may be worth is through a formal review. This typically involves:

- Basic policy information

- Authorization to review medical records

- A preliminary valuation

Understanding your potential payout can help you make an informed decision about whether selling makes sense. To learn if you are likely to qualify for a viatical settlement or life settlements, please give us a call at 800-973-8258.