An Educational Consumer Guide from Viatical.org

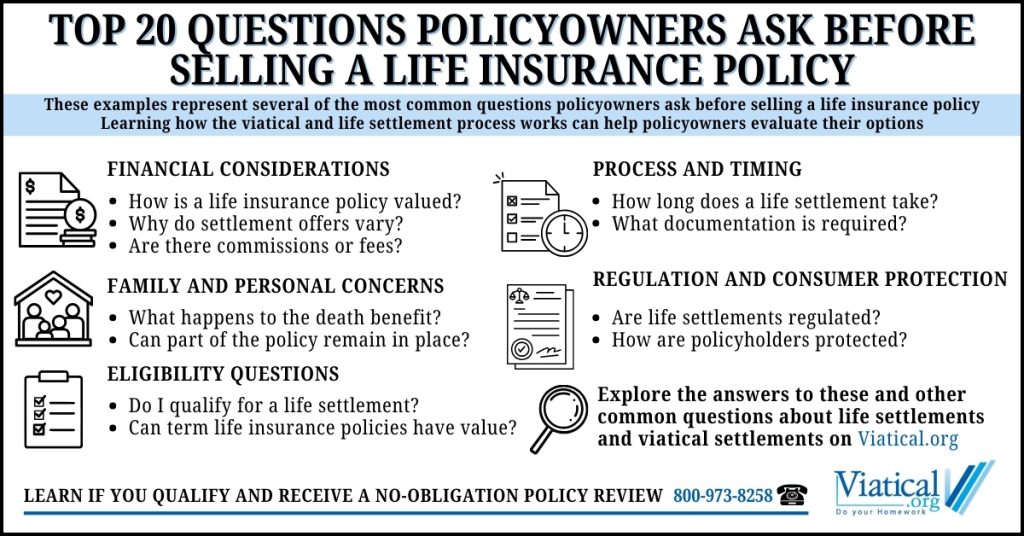

The following guide addresses the top 20 questions policyowners ask before selling a life insurance policy.

Most people purchase life insurance during a period of responsibility.

A growing family. A mortgage. Estate planning. Business protection. The policy represents long-term security for people who depend on you. Premiums are paid faithfully for years, often decades, with the expectation that the death benefit will someday fulfill its purpose.

But life changes.

Children become financially independent. Retirement replaces earned income. Health circumstances evolve. Premium obligations increase. Policies that once made perfect financial sense can slowly become difficult to maintain.

What many consumers never learn is that a life insurance policy is legally recognized property. Under U.S. law, it may be sold through a regulated secondary market known as a life settlement or viatical settlement.

The U.S. Government Accountability Office found that many policyholders allow coverage to lapse without realizing their policies may have measurable resale value in this regulated marketplace (GAO-10-775).

This guide addresses the real questions policyholders ask before considering that option.

Many people simply want to understand whether their policy has value before deciding what to do next. A confidential policy appraisal often answers that question quickly, without obligation or pressure.

1. What if selling my life insurance policy deprives my loved ones of the death benefit I worked so hard to secure?

Life insurance is rarely purchased casually. It reflects years of responsibility toward spouses, children, or business partners. Selling coverage means ownership transfers to a buyer who assumes future premium payments and ultimately receives the death benefit.

That reality should never be minimized. However, most policies evaluated for life settlements are already facing a different risk: lapse. According to federal analysis by the Government Accountability Office, large numbers of policies terminate without paying any benefit because premiums eventually become unaffordable or unnecessary for changing family needs.

When lapse occurs, beneficiaries receive nothing despite years of payments.

A life settlement changes that outcome by allowing the policyholder to access value while living rather than losing the policy entirely.

Importantly, selling coverage does not always have to be an all-or-nothing decision. Certain larger policies may qualify for retained death benefit structures, allowing part of the insurance to remain in place for beneficiaries while still generating immediate liquidity.

Many families ultimately view the decision not as removing protection, but adapting financial planning to present realities.

If uncertainty exists, beginning with a policy appraisal allows discussion before any permanent decision is made.

2. How is my policy actually valued, and why do offers vary so much?

One of the most misunderstood aspects of life settlements is valuation.

There is no universal resale price for life insurance policies. Settlement value depends on long-term actuarial analysis performed by licensed buyers evaluating investment risk.

Primary factors include:

- Life expectancy projections derived from medical underwriting

- Ongoing premium obligations

- Policy type such as universal life, whole life, or convertible term

- Carrier financial strength

- Interest rate assumptions

- Policy guarantees and conversion rights

Because each institutional purchaser applies different actuarial models, offers can vary significantly for the same policy. This variation is normal.

The National Association of Insurance Commissioners (NAIC), which develops model consumer protection laws adopted by most states, recognizes that life settlement transactions involve independent valuation by licensed providers operating under regulated disclosure standards.

The most effective consumer protection is understanding value early through appraisal rather than negotiation under pressure.

3. Am I at risk of receiving a low offer if only one buyer reviews my policy?

Potentially, yes.

Unlike publicly traded investments, life settlements operate through negotiated institutional markets. A single offer reflects only one buyer’s internal assumptions about longevity risk and premium exposure.

Without competitive review, policyholders may never know whether another licensed purchaser would value the policy differently.

At the same time, consumers understandably worry about widespread sharing of medical information.

Federal medical privacy protections under the HIPAA Privacy Rule, administered by the U.S. Department of Health and Human Services, strictly govern how protected health information may be disclosed during financial and insurance transactions.

Modern settlement platforms attempt to balance both concerns by securely presenting policy information only to licensed entities actively reviewing qualified policies.

The goal is informed evaluation, not unnecessary exposure.

4. Won’t broker commissions consume up to 30% of my payout?

This is one of the most important questions consumers ask, and candid discussion matters.

Many traditional life settlement brokers are compensated through commissions tied to the gross settlement amount. Depending on structure and disclosure requirements, compensation can approach 30 percent in some transactions.

The NAIC Viatical Settlements Model Act specifically requires disclosure of compensation arrangements so policyholders understand how intermediary fees affect proceeds.

Broker agreements may also include exclusivity provisions limiting alternative offers for a defined period.

Consumers considering brokerage representation should understand compensation terms fully before signing agreements and may wish to exclude any independent or direct offers they plan to review separately.

Understanding net proceeds rather than headline offers helps policyholders evaluate outcomes realistically.

5. What if shady characters or “Tony Soprano” types end up owning my policy?

Nobody wants their life insurance policy sitting in Tony Soprano’s IRA.

It sounds humorous, but the concern is real. People understandably worry about who ultimately profits from their policy after sale.

In reality, modern life settlements are typically funded by institutional investors such as pension funds, university endowments, and regulated asset managers seeking long-duration financial assets.

State insurance regulation requires licensing of life settlement providers and imposes consumer disclosure protections governing transactions. The NAIC model framework adopted by most states establishes these safeguards.

Policies are generally pooled within institutional investment funds rather than owned by individuals.

Understanding this institutional structure often replaces discomfort with clarity about how the secondary market actually operates.

6. What happens if my insurance company later goes out of business?

Once a settlement transaction closes and the rescission period expires, responsibility for the policy transfers entirely to the new owner.

You are no longer responsible for premium payments or future carrier risk apart from fraud at origination.

Life insurance companies operate under state solvency oversight supported by guaranty association protections designed to maintain contractual obligations even if an insurer encounters financial difficulty. The Federal Insurance Office outlines this regulatory framework within U.S. insurance supervision.

If anything happens to the insurer after sale, that risk belongs to the buyer, not the seller.

Your proceeds remain unaffected.

7. Are there significant tax implications or impacts on my government benefits if I sell my life insurance policy?

This is one of the most important questions to address before moving forward with any life settlement or viatical settlement.

The short answer is that when you sell your life insurance policy for cash, tax treatment depends heavily on individual circumstances, which is why careful planning matters.

In general, proceeds received from selling a life insurance policy are divided into components for tax purposes. Amounts received up to the total premiums you paid into the policy, often referred to as your cost basis, are typically treated as a return of your own money. Amounts received above that level may be taxable depending on how the policy performed and how long it was held.

However, qualified viatical settlements involving individuals who are terminally or chronically ill are frequently treated differently under federal law. The Internal Revenue Code allows certain viatical settlement proceeds to be excluded from taxable income when medical certification requirements are met under accelerated death benefit rules established by Congress.

While this tax advantage can be significant, another consideration is how a lump-sum payment may affect eligibility for needs-based programs such as Medicaid or Supplemental Security Income. Government benefit programs often evaluate available assets when determining eligibility.

The Centers for Medicare & Medicaid Services explains that financial resources can influence qualification thresholds for certain assistance programs.

For this reason, policyholders frequently consult tax professionals or elder-law attorneys before completing a transaction. Understanding potential net proceeds after taxes or benefit adjustments allows decisions to be made thoughtfully rather than reactively.

Many individuals begin simply by obtaining a policy appraisal to understand possible settlement ranges before exploring planning strategies.

8. Will my privacy be invaded with constant health inquiries from the new owner after I sell?

This concern is extremely common, and it is reasonable.

When someone sells a life insurance policy, the buyer assumes responsibility for future premiums and therefore has a financial interest in monitoring life expectancy projections over time. That monitoring requires occasional confirmation of health status.

What many people imagine, however, is far different from what actually occurs.

Policyholders are not contacted constantly, and buyers themselves typically do not reach out directly. Instead, licensed servicing companies handle periodic updates under strict privacy requirements governed by federal law.

The HIPAA Privacy Rule, administered by the U.S. Department of Health and Human Services, regulates how protected health information may be requested, stored, and shared.

In practice:

- Traditional life settlements usually involve one brief check-in once or twice per year.

- Viatical settlements may involve somewhat more frequent contact due to medical circumstances.

Most communications consist of short confirmation requests rather than detailed medical examinations. Policyholders are not required to provide ongoing medical testing or intrusive disclosures beyond previously authorized updates.

Understanding this administrative requirement ahead of time helps remove uncertainty. Most sellers later describe the process as routine rather than burdensome.

9. Is the process of selling life insurance too complex or risky compared to simply surrendering the policy?

From the outside, the settlement process can appear intimidating.

Medical records must be reviewed. Insurance carriers must verify coverage. Legal disclosures must be signed. Offers must be evaluated. Compared to calling an insurance company and requesting surrender paperwork, the process understandably seems more involved.

The reason for that complexity is consumer protection.

State-regulated life settlement transactions include mandatory disclosures, escrow requirements, anti-fraud safeguards, and rescission periods allowing policyholders to reverse the transaction after payment if they change their mind.

These protections exist because ownership of a financial asset is permanently transferring.

The National Association of Insurance Commissioners (NAIC) developed the Viatical Settlements Model Act specifically to establish disclosure standards, licensing requirements, and consumer safeguards adopted by most states.

By comparison, surrendering a policy is simple precisely because the insurance company already controls the transaction.

Many policyholders ultimately discover that a slightly more structured process provides substantially greater financial outcome than surrendering coverage for limited cash value or allowing lapse.

A common first step is simply determining whether meaningful settlement value exists before deciding whether additional effort is worthwhile.

10. What if my health improves or I regret selling my life insurance later? Will I be locked out of coverage forever?

This concern reflects a very human hesitation about making permanent financial decisions.

A life settlement does permanently transfer ownership of the existing policy. Once completed and the rescission period expires, the policy cannot be reclaimed.

However, selling one policy does not prevent someone from purchasing life insurance again in the future.

Individuals remain free to apply for new coverage at any time, subject to normal underwriting based on age and health at that point. Some policyholders who sell coverage later obtain smaller or more affordable policies aligned with updated financial needs.

It is also important to understand that not every policy sold results from declining health. Some perfectly healthy individuals sell policies because premiums have increased dramatically, estate planning goals have changed, or convertible policy provisions create market value independent of medical condition.

The decision therefore becomes less about losing insurance forever and more about evaluating whether the current policy still serves its original purpose.

Taking time to understand options through appraisal or discussion often helps policyholders reach decisions with greater confidence and less second-guessing later.

11. How can there be value in a term life insurance policy that has no cash value?

Many policyholders are surprised to learn that certain term life insurance policies may still have resale value, even though they do not accumulate traditional cash value.

The key factor is convertibility.

Some term policies include contractual provisions allowing the policyholder to convert coverage into permanent insurance, such as universal life or whole life, without undergoing new medical underwriting. That conversion right can become extremely valuable if health has declined since the policy was originally issued.

From a buyer’s perspective, the ability to convert coverage without additional medical risk creates future certainty. Even though the policy itself does not currently contain cash value, the conversion privilege may allow long-term maintenance of coverage.

In certain situations, particularly where health impairment exists, buyers may be willing to purchase convertible term policies before expiration. Annual renewable term policies may also qualify, although eligibility often depends on age, premium structure, and medical condition.

Many consumers mistakenly assume their expiring term policy is worthless and allow coverage to lapse. Federal consumer research has noted that policyholders frequently lack awareness of secondary market options before terminating coverage.

Settlement proceeds received up to total premiums paid are generally treated as return of basis for tax purposes.

A simple appraisal often determines whether a term policy contains hidden value before expiration eliminates available options entirely.

12. What exactly is the difference between a life settlement and a viatical settlement?

Although the terms are sometimes used interchangeably, they describe related but distinct transactions.

A life settlement generally involves older policyholders, often age 65 or above, who no longer need or wish to maintain life insurance coverage. Health status may influence valuation but is not always the determining factor.

A viatical settlement, by contrast, applies when the insured individual has been medically certified as chronically or terminally ill. Because life expectancy is shorter, buyers assume fewer future premium obligations, which often results in higher settlement percentages relative to the death benefit.

Federal tax law recognizes this distinction. Qualified viatical settlement proceeds may be treated similarly to accelerated death benefits and excluded from taxable income when statutory requirements are met.

Both transactions follow the same general structure:

- Ownership transfers to a licensed buyer

- The buyer assumes future premium payments

- The policyholder receives a lump-sum payment

- The buyer receives the death benefit in the future

Understanding which category applies helps policyholders evaluate timelines, taxation, and expected settlement ranges.

Many individuals begin simply by determining whether their circumstances qualify for one category or the other before exploring next steps.

13. Do I need to be terminally ill to receive cash for my life insurance policy?

No, and this is one of the most persistent misconceptions surrounding settlements.

While viatical settlements specifically involve serious medical conditions, life settlements are commonly completed by seniors who are not terminally ill. Age, premium burden, and policy structure alone may create market value.

Institutional buyers evaluate policies based on overall investment characteristics rather than diagnosis alone. Factors such as rising premiums, universal life funding requirements, or estate planning changes frequently lead otherwise healthy policyholders to explore settlements.

The NAIC consumer framework governing life settlements recognizes eligibility beyond terminal illness and establishes disclosure requirements designed to ensure policyholders understand available alternatives before terminating coverage.

In practice, many callers are surprised to learn they may qualify despite relatively stable health.

Understanding eligibility begins with reviewing policy details rather than assuming disqualification.

14. Are there minimum age or policy size requirements?

While there is no universal rule, general industry patterns exist.

Most institutional buyers prefer:

- Insured individuals age 65 or older

- Policies with face amounts of $100,000 or greater

- Permanent insurance such as universal or whole life

- Convertible term policies approaching expiration

However, exceptions occur frequently. Younger insured individuals with significant health impairment may qualify, and some large policies may attract buyer interest depending on life expectancy and policy structure.

Settlement qualification ultimately depends on underwriting evaluation rather than rigid thresholds.

State regulatory frameworks require licensed providers to evaluate policies individually and disclose relevant transaction details to consumers before completion.

Because eligibility varies widely, many policyholders begin with appraisal simply to determine whether review is worthwhile.

15. How long does the life settlement or viatical settlement process usually take?

Timing depends on several factors, including medical record availability, carrier responsiveness, and underwriting complexity.

A typical life settlement transaction may take between 30 and 90 days from initial review to funded escrow. Viatical settlements involving serious illness often proceed more quickly due to urgency, sometimes completing within several weeks.

The general process includes:

- Policy appraisal and preliminary review

- Medical underwriting

- Policy verification with the insurance carrier

- Offer presentation

- Contract execution

- Escrow funding

- Rescission period allowing cancellation after payment

Consumer protection laws require rescission periods, usually ranging from 15 to 30 days depending on state regulation, allowing policyholders to reverse the transaction after receiving funds if they reconsider.

These safeguards are incorporated into state settlement laws modeled after NAIC standards designed specifically to protect sellers during ownership transfer.

While the process requires patience, most policyholders find the structured timeline manageable once expectations are understood.

16. What documentation and steps will I actually need to complete if I decide to explore selling my policy?

One reason policyholders hesitate to explore a life settlement or viatical settlement is the assumption that the process will involve overwhelming paperwork or medical intrusion.

In reality, most of the required documentation already exists.

Typical items include:

- An in-force illustration or policy statement from the insurance carrier

- Identification verification

- Authorization allowing medical record review

- Settlement disclosures required by state law

Medical underwriting is necessary because buyers must evaluate life expectancy projections. However, policyholders are rarely responsible for gathering records themselves. Authorized requests are typically handled through structured processes designed to comply with federal privacy protections.

The HIPAA Privacy Rule, administered by the U.S. Department of Health and Human Services, governs how medical information may be requested and transmitted during financial transactions involving insurance assets.

Most participants find that their involvement consists primarily of reviewing disclosures and providing signatures rather than coordinating multiple institutions independently.

Understanding what is actually required often removes one of the largest perceived barriers to simply learning whether a policy qualifies.

17. How do state regulations and licensing laws protect me during a life settlement transaction?

Life settlements are not informal financial arrangements. They are regulated insurance transactions governed primarily at the state level.

Nearly every state has adopted laws modeled after the NAIC Viatical Settlements Model Act, which establishes licensing standards, disclosure requirements, privacy protections, and consumer rights.

These protections typically include:

- Licensing requirements for life settlement providers

- Mandatory written disclosures explaining alternatives

- Anti-fraud provisions

- Escrow requirements ensuring payment security

- Defined rescission periods allowing cancellation after payment

These safeguards exist because the transaction permanently transfers ownership of a valuable financial asset.

Consumers should verify that any party involved in a settlement is properly licensed within their state. State insurance departments maintain licensing databases specifically for this purpose.

Regulation does not eliminate every risk, but it provides meaningful oversight designed to protect policyholders throughout the transaction process.

18. Can I sell multiple policies or only one at a time?

Many policyholders hold more than one life insurance policy acquired over different stages of life.

There is generally no requirement limiting settlement review to a single policy. Multiple policies across different carriers may be evaluated simultaneously.

In some situations, reviewing policies together provides a clearer financial picture. Institutional buyers often assess overall premium exposure and policy structure collectively rather than individually.

Options may include:

- Selling one policy while retaining another

- Selling portions through retained death benefit arrangements

- Monetizing policies that are nearing lapse while maintaining essential coverage

Because policies serve different purposes, decisions are rarely uniform across all coverage.

Beginning with a comprehensive review allows policyholders to understand how each policy fits within broader retirement planning, estate planning, or long-term care funding goals.

19. Can life settlement proceeds help pay for medical care, long-term care, or retirement expenses?

Settlement proceeds are unrestricted funds. Once payment is received through escrow and the rescission period expires, the policyholder may use the money for any purpose.

Common uses include:

- Long-term care expenses

- Assisted living or in-home care

- Medical treatments not fully covered by insurance

- Debt reduction

- Retirement income supplementation

- Family support or travel

The U.S. Department of Health and Human Services recognizes long-term care costs as one of the most significant financial challenges facing aging Americans.

For some individuals, converting an underperforming insurance asset into liquid funds provides flexibility unavailable through traditional financing options.

However, large lump-sum payments may affect eligibility for certain needs-based assistance programs. Advance planning with financial or legal advisors can help minimize unintended consequences.

Understanding potential settlement value first allows planning decisions to occur with accurate information rather than speculation.

20. How do I make sure I receive a fair offer and choose the right path forward?

This final question often reflects everything that came before it.

Policyholders want reassurance that they are making an informed decision, not reacting to pressure or incomplete information.

Several practical steps help protect consumers:

- Confirm all participating entities are properly licensed

- Understand compensation structures before signing agreements

- Avoid unsolicited or high-pressure solicitations

- Compare offers where appropriate

- Take time to review disclosures carefully

Federal and state regulators consistently emphasize informed consent and transparency as central consumer protections within life settlement markets.

For many individuals, the most prudent first step is not selling a policy at all, but simply determining whether it has value.

That is why many policyholders begin with a confidential appraisal or conversation to ask questions before deciding anything further.

Knowledge reduces uncertainty. Options create confidence.

Exploring Your Options

Life insurance is purchased with long-term intention, but financial planning does not end the day a policy is issued.

Changing health conditions, retirement realities, rising premiums, and evolving family needs can transform a once-essential policy into an underused financial asset. Allowing coverage to lapse or surrendering it without evaluation may unintentionally forfeit meaningful value.

Life settlements and viatical settlements exist precisely because policies represent property rights recognized under law. When conducted through licensed entities within regulated frameworks, they provide an additional option alongside maintaining or surrendering coverage.

At Viatical.org, our mission is not to encourage any single outcome. It is to ensure policyholders understand their choices.

Some individuals ultimately keep their policies.

Others surrender coverage.

Many simply appreciate learning that another option existed.

A policy appraisal or conversation often answers questions more clearly than speculation. There is no obligation to proceed, and asking questions carries no cost.

Understanding your options today may prevent regret tomorrow. Please give us a call today to learn if you are likely to qualify and for a no-obligation policy appraisal. 800-973-8258