For many seniors and their families, the rising cost of extended medical support can be overwhelming. Nursing homes, assisted living facilities, and in-home caregivers often come with monthly bills that quickly drain savings. Fortunately, there are alternatives to simply spending down retirement accounts. One option is using life insurance to pay for long-term care, which allows policyholders to convert an existing life insurance policy into funds that can be applied toward these expenses.

Why Long-Term Care Costs Are a Concern

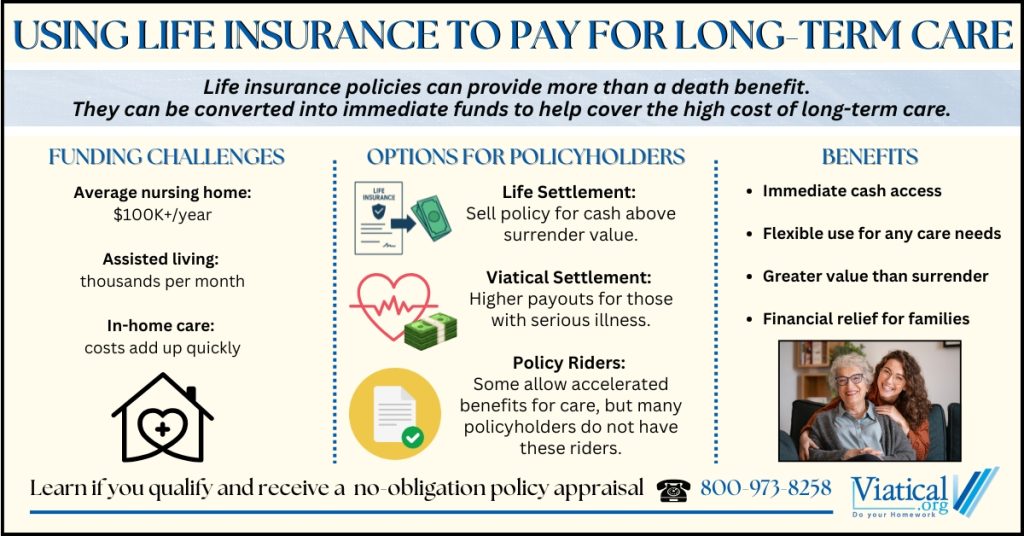

Long-term care is not covered by Medicare in most situations, and private health insurance rarely offers comprehensive coverage for extended care. According to national surveys, the average cost of a private room in a nursing home exceeds $100,000 per year. Even assisted living or in-home care services can reach thousands of dollars per month. These expenses often leave families in difficult financial positions, searching for new sources of funding.

How Life Insurance Fits into the Picture

Many people are unaware that a life insurance policy is considered an asset that can be sold or converted for cash. Instead of surrendering a policy for a small cash value or allowing it to lapse, policyholders can use it to help pay for care. Options include:

- Life Settlements: Seniors age 65 or older with life insurance may sell their policy to a licensed buyer for more than the surrender value. The buyer takes over premium payments and the policyholder receives a lump sum of cash. Funds from life settlements can be used for any purpose, including long-term care.

- Viatical Settlements: For individuals with serious or terminal health conditions, a viatical settlement may provide immediate access to a higher payout. These transactions are designed specifically for people facing major health challenges and insureds younger than 65 can qualify as health status, rather than age, is most important.

- Hybrid Products and Riders: Some policies include long-term care riders, which allow the policyholder to accelerate a portion of their death benefit to pay for care costs while they are still alive. Not all policies offer this feature, but it’s worth checking the details with the insurer.

Benefits of Converting Life Insurance for Care Costs

Choosing to use a life insurance policy for care-related expenses offers several advantages:

- Immediate access to funds: Rather than waiting for the death benefit, families can use cash now to secure quality care.

- No restrictions on use: Settlement funds can be applied to nursing homes, home care services, assisted living, or other medical needs.

- Higher value than surrender: In many cases, selling a policy provides significantly more than the insurance company’s surrender payout.

- Relief for families: Accessing funds through life insurance can reduce financial pressure on adult children or spouses who may otherwise have to cover the cost of care.

Who Qualifies?

Not every policyholder will qualify for a life settlement or viatical settlement, but many seniors are eligible. Typical factors include:

- Policy type: Universal, whole, and convertible term policies most commonly qualify though even Group policies can qualify and non-convertible term policies in some cases.

- Policy size: Policies usually must have a face value of $100,000 or more.

- Age and health: Older individuals or those with declining health usually receive higher offers. For life settlements, the insured is usually 65 or older. Younger insureds can qualify for viatical settlements.

Even if you are not sure whether your policy qualifies, it is often worth exploring your options.

Steps to Get Started

If you are considering this path, here are a few steps to take:

- Review your policy: Gather details such as policy type, face value, and premium costs.

- Request an appraisal: A professional life settlement appraisal can provide an estimate of what your policy may be worth in today’s secondary market.

- Consider your offer: If your policy qualifies, you may receive an offer from a direct buyer. Decide if you would like to accept.

- Plan for care needs: Decide how the funds will be used, whether for immediate nursing support, assisted living, or in-home care.

A Practical Alternative for Long-Term Care Funding

Traditional options for paying long-term care costs include savings, long-term care insurance, or Medicaid after assets are depleted. However, using life insurance to pay for long-term care can provide another path, one that unlocks hidden value in an existing policy. For families struggling with high medical bills and care expenses, this option can bring financial relief while ensuring loved ones receive the quality care they deserve.

To learn if you or your loved one qualify and receive a no-obligation policy appraisal, please give us a call at 800-973-8258. We’ll help you understand if you’re able to access value in your policy today to pay for long-term care needs.