If you are wondering what happens if you stop paying life insurance premiums, the outcome depends on the type of policy you own, how long premiums have gone unpaid, and whether any options are exercised before the policy lapses. Many policyholders stop paying premiums during illness, retirement, or financial stress without realizing that doing so can permanently eliminate valuable rights. Understanding the timeline and consequences can help you avoid losing coverage or policy value unnecessarily.

The Grace Period After a Missed Payment

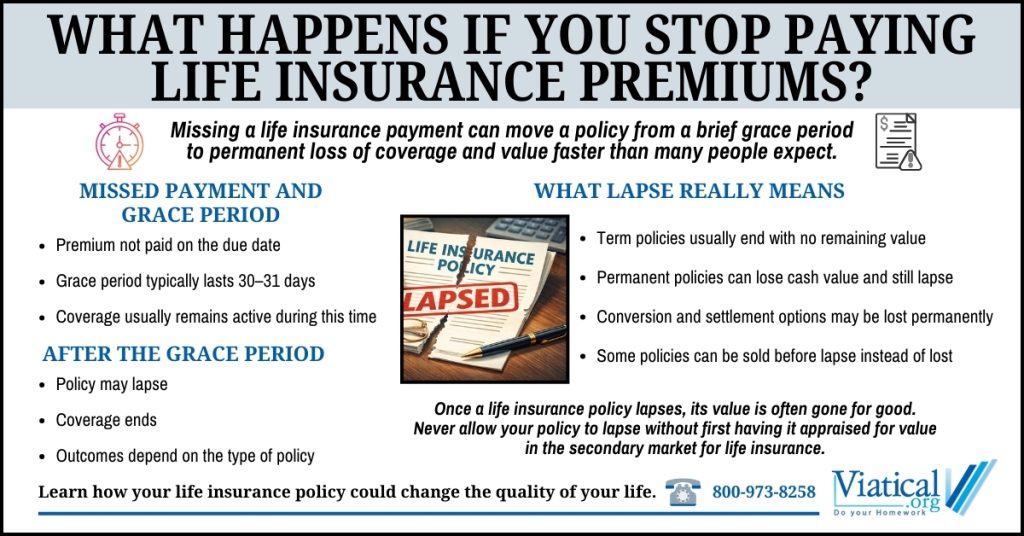

Most life insurance policies include a grace period, typically 30 or 31 days. During this time, coverage usually remains in force even though a payment has been missed.

- If the premium is paid within the grace period, the policy continues as normal.

- If the insured passes away during the grace period, the insurer generally pays the death benefit minus the overdue premium.

Once the grace period ends, the consequences change quickly.

What Happens After the Grace Period Ends

When premiums remain unpaid beyond the grace period, the policy may lapse. A lapse means the policy is no longer active, and coverage stops.

What happens next depends on the policy type.

Term Life Insurance Policies

With term life insurance:

- The policy usually lapses entirely.

- Coverage ends with no payout or residual value.

- Conversion rights tied to the policy may be lost once the policy lapses.

This is particularly important for older insureds or those with health conditions, since conversion options may allow access to value that disappears after lapse.

Permanent Life Insurance Policies

Permanent policies such as whole life and universal life often have additional mechanisms that delay or soften the impact of missed payments.

Possible outcomes include:

- Automatic premium loans using policy cash value

- Reduced cash value as internal charges continue

- Policy lapse once available cash value is depleted

Although permanent policies may last longer without payments, they can still terminate if no action is taken.

Reinstatement May Be Possible but is Not Guaranteed

Many policies allow reinstatement within a specific window, often two to five years after lapse. Reinstatement usually requires:

- Payment of past-due premiums

- Interest on unpaid amounts

- Evidence of insurability

If health has declined, reinstatement may be denied or financially impractical.

Loss of Value When a Policy Lapses

When a policy lapses, you may lose:

- Conversion rights

- Settlement eligibility

- Cash value growth

- The ability to use the policy for financial planning or care expenses

Once a lapse occurs, these losses are often irreversible.

Alternatives to Letting a Policy Lapse

Before stopping premium payments, policyholders may have options that preserve value. These can include:

- Adjusting premium structures

- Reducing the face amount

- Using existing cash value strategically

- Exploring whether the policy can be sold instead of lapsing

For eligible policies, selling your life insurance policy may allow access to funds while relieving the burden of ongoing premiums.

Why Timing Matters

The window between missing a payment and full lapse is often the last opportunity to act. Once the policy terminates, the ability to recover value is extremely limited.

This is especially relevant for individuals who:

- Are no longer able to work

- Are facing medical expenses

- Have outlived the original need for coverage

- Own policies that are becoming unaffordable

Making an Informed Decision

Stopping premium payments may seem like a simple way to reduce expenses, but it can result in the permanent loss of a valuable asset. Reviewing your policy type, grace period, and available alternatives before allowing a lapse can make a significant difference.

Understanding what happens if you stop paying life insurance premiums allows you to make a deliberate choice rather than losing coverage or value by default. Always have your life insurance policy appraised for value in the life settlement market prior to allowing it to lapse. This way, you can avoid throwing away any hidden value.

To learn if you qualify to sell all or a portion of your policy for cash, please give us a call at 800-973-8258.