Policyowners often wonder what their options are if they no longer want to keep paying premiums on a life insurance policy. One of the most common questions people ask is what types of life insurance policies can be sold for cash. In many situations, life settlements or a viatical settlement allow a policyholder to sell an existing policy to a licensed purchaser in exchange for a lump-sum payment. The purchaser then becomes responsible for future premium payments and receives the death benefit when the insured passes away.

While not every policy will qualify, many types of life insurance coverage may be eligible for sale in the secondary market.

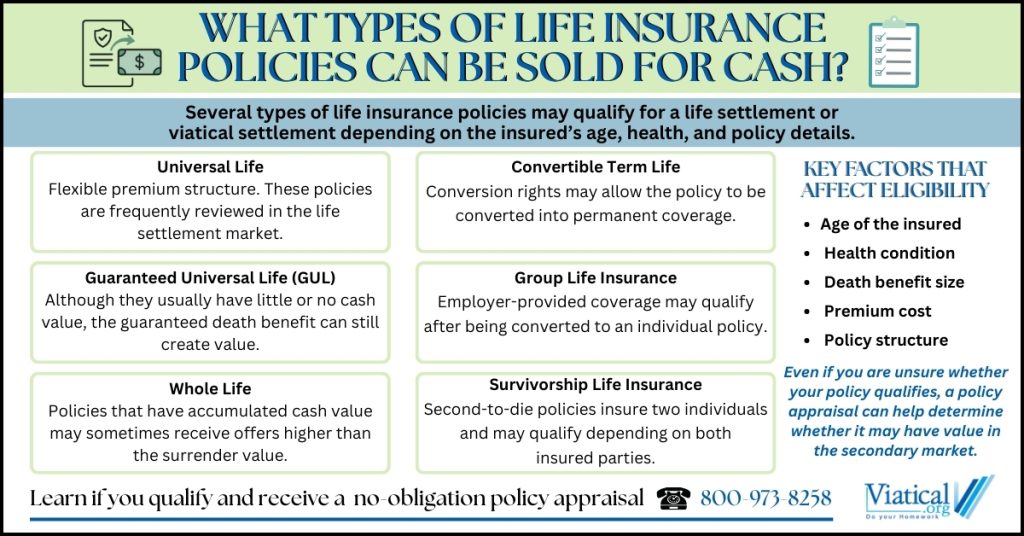

Universal Life Policies

Universal life insurance policies are among the most frequently sold policies in life settlements. These policies offer flexible premium structures and remain in force as long as sufficient funds are available to support the coverage.

As the insured gets older, universal life policies can become increasingly expensive to maintain. Rising insurance costs within the policy may require higher premium payments to keep the coverage active. When policyowners no longer want the policy or find the premiums difficult to maintain, selling the policy can provide an alternative to surrendering it to the insurance company.

Most buyers require a minimum death benefit of around $100,000, although policies with substantially larger face values tend to attract greater interest.

Guaranteed Universal Life (GUL) Policies

Guaranteed Universal Life policies, commonly referred to as GUL policies, are designed to provide a guaranteed death benefit until a specific age such as 90, 95, or 100 as long as required premiums are paid.

Unlike many traditional universal life policies, GUL policies usually accumulate little or no cash value. However, they can still qualify for a life settlement because the guaranteed death benefit can be attractive to purchasers in the secondary market. Even though surrendering a GUL policy to the insurance company may produce little or no cash value, the policy may still hold value if the insured’s health or age meets certain criteria.

Whole Life Insurance

Whole life insurance policies may also be sold for cash through a life settlement. These policies build guaranteed cash value over time and generally require fixed premium payments.

If the policyowner decides the coverage is no longer necessary, the insurance company may allow the policy to be surrendered for its accumulated cash value. However, settlement purchasers may sometimes offer far more than the surrender value because they intend to maintain the policy and collect the full death benefit later.

Convertible Term Life Insurance

Term life insurance policies may also be eligible to be sold if they include a conversion privilege. Convertible term policies allow the policyholder to convert the coverage into permanent life insurance, such as universal life, without undergoing a new medical exam.

Even though term policies generally do not build cash value, the conversion feature can create value for settlement purchasers. The buyer may convert the policy to permanent coverage and continue maintaining it over time.

It is always best to have your policy appraised at least 6 months prior to the end of your conversion privilege as premiums often rise sharply after the initial term, making the policy unattractive to buyers. In some situations, even non-convertible term policies can be sold, but this usually occurs only when the insured qualifies for a viatical settlement due to a serious medical condition.

Group Life Insurance

Group life insurance policies provided through an employer can sometimes be sold as well, although they often require additional steps.

In many cases, the employee must first convert the group coverage to an individual policy before it becomes eligible for a life settlement. Conversion rights often apply when an employee retires, changes jobs, or leaves the employer that provided the coverage.

Once converted to an individual policy, the coverage may qualify for a life settlement depending on factors such as the insured’s age, health condition, and the size of the death benefit.

Survivorship (Second-to-Die) Life Insurance

Survivorship life insurance policies, also called second-to-die policies, insure two individuals and pay the death benefit only after both insured parties have passed away. These policies are often used for estate planning purposes.

Although survivorship policies can sometimes be sold, they are evaluated differently from policies covering a single insured person. Buyers analyze the health and life expectancy of both insured individuals when determining whether the policy may qualify for a life settlement.

Every Policy Is Unique

While the policy types above are commonly sold in life settlements, every situation is different. The insured’s age, overall health, policy size, premium cost, and policy structure all influence whether a policy may qualify.

Because of these variables, it is not always possible to determine eligibility based on policy type alone. Even policies that initially appear unlikely to qualify may still have value depending on the circumstances.

Policyowners should have their policy appraised to determine whether it may hold value in the secondary market. Many policies that people assume have little or no value may still attract interest from life settlement buyers under the right conditions.

Understanding what types of life insurance policies can be sold for cash helps policyowners recognize that their policy may represent a financial asset rather than simply an expense. When coverage is no longer needed or premiums have become difficult to maintain, obtaining a policy appraisal can reveal whether that policy may be converted into cash while the policyholder is still living.

To learn if you are likely to qualify and for a no obligation policy appraisal, please give us a call at 800-973-8258. We have been helping policyowners learn about their options for accessing the hidden value in life insurance for over 20 years.