If you’ve been diagnosed with a terminal illness and have an active life insurance policy, you may be wondering: Who qualifies for a viatical settlement in 2025? This option, which allows individuals to sell their life insurance policy to a viatical settlement buyer for a lump-sum cash payment, continues to provide a critical financial lifeline for those facing high medical costs or needing to stabilize their finances during a difficult time.

Viatical settlements are not new, but recent industry data shows that more people are turning to this option—and receiving significant payouts.

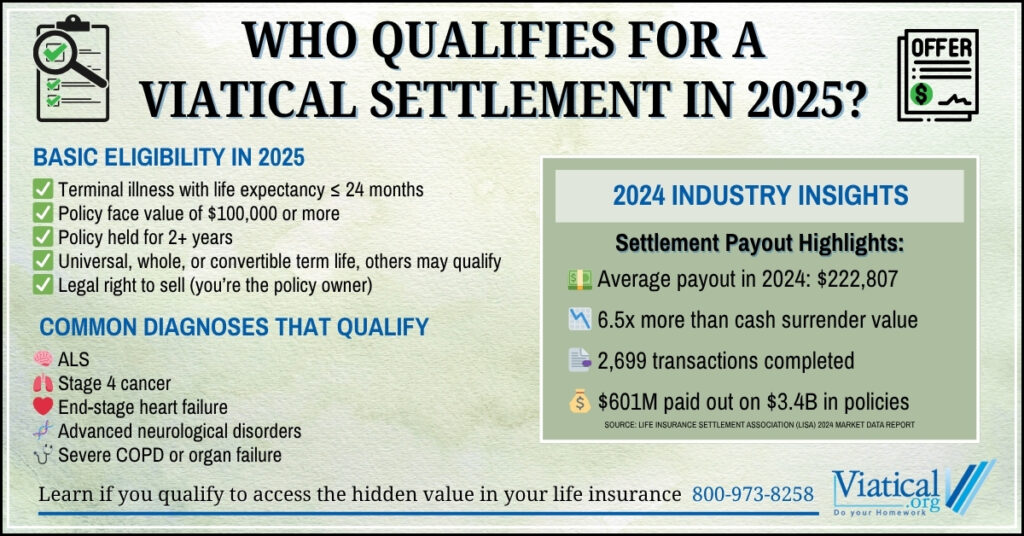

Updated Market Data: What You Should Know

According to the 2024 Market Data Report from the Life Insurance Settlement Association (LISA):

- The average payout for a life settlement in 2024 was $222,807.

- On average, this amount was 6.5 times higher than the policy’s cash surrender value.

- A total of 2,699 life settlement transactions were completed by LISA members in 2024.

- These transactions represented $3.4 billion in face value and resulted in over $601 million in total payments to consumers.

While this data includes both viatical and traditional life settlements, it highlights the growing financial benefits of selling a life insurance policy—especially for those who qualify due to terminal illness.

Basic Eligibility Criteria in 2025

To qualify for a viatical settlement in 2025, you’ll generally need to meet the following requirements:

1. Terminal Illness Diagnosis

Most buyers require that the insured individual has a life expectancy of 24 months or less. Common qualifying conditions include late-stage cancer, ALS, advanced heart failure, and other life-limiting diagnoses. Each case is evaluated individually.

If you have a longer life expectancy and are 65 or older, you may qualify for life settlements which still allow you to access the hidden value in your life insurance policy.

2. Policy Type

Viatical settlements are available for a variety of life insurance policies, including:

- Universal Life

- Whole Life

- Convertible Term Life

- In some cases, even group life policies or non-convertible term policies may qualify.

3. Policy Age and Size

- The policy must typically be at least two years old.

- Most buyers prefer a face value of $100,000 or more, though smaller policies may still qualify depending on health status and policy structure.

4. Policy Ownership

You must have the legal right to sell the policy—either as the owner or through proper documentation if the policy is owned by a trust or business entity.

Why More People Are Exploring This Option

The dramatic difference between viatical settlement payouts and surrender values is one of the key reasons individuals with terminal diagnoses are considering this option in 2025. When policyholders are faced with financial pressure, especially for out-of-pocket medical expenses, the ability to receive six times more than their insurance carrier would offer as a surrender value can be life-changing.

As the viatical settlement market continues to grow, more patients and families are becoming aware of this alternative. If you or a loved one has a qualifying diagnosis and an unwanted or unneeded life insurance policy, it’s worth looking into a viatical settlement.

To learn if you qualify and receive a no-obligation policy appraisal, please give us a call at 800-973-8258. Every case is different, so it is always best to call to learn your options.