Families across the country face the challenge of covering the high costs of in home care services and other types of senior care services. One option often overlooked is paying for in home care services with term life insurance. While term coverage is usually seen as a way to leave a death benefit, under the right circumstances, it can also be converted into a valuable source of immediate funds to help pay for essential care.

The Rising Cost of In-Home Care

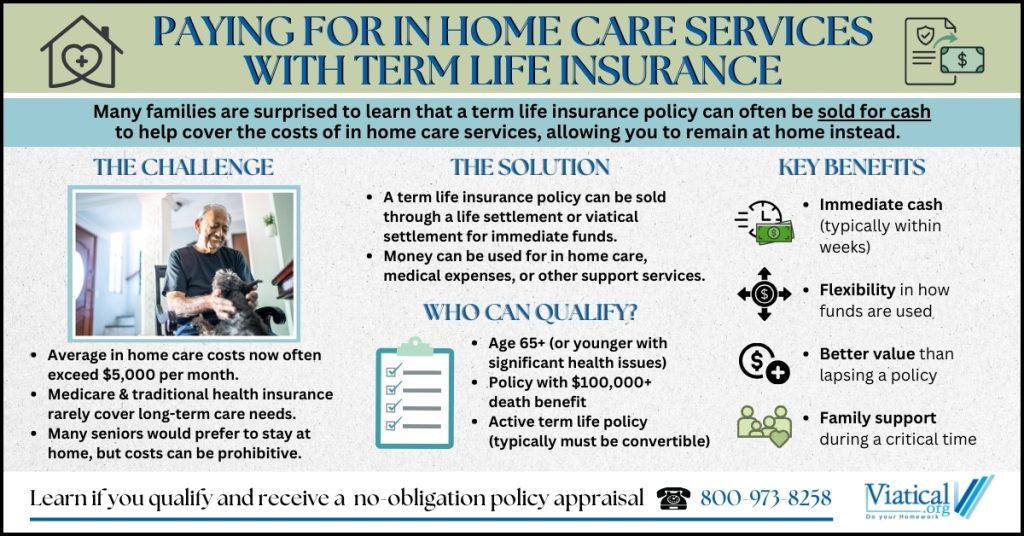

The demand for in home senior care continues to grow as many older adults prefer to remain at home with the help of a home care agency or private in home caregiver, rather than move into a nursing facility. According to industry reports, the average cost of a home health aide now exceeds $5,000 per month.

Whether families hire home health agencies or choose well-known providers such as Visiting Angels Home Care or Home Instead Senior Care, the monthly expenses can quickly overwhelm a household budget. Medicare and traditional health insurance rarely cover these long-term needs, leaving families searching for practical funding alternatives.

Turning Term Life Insurance into Cash

Most people think of term life insurance as expiring without value if the insured outlives the policy term. However, there is a way to unlock financial benefit while still alive if you qualify – selling the policy through a life settlement.

A life settlement is the sale of a life insurance policy to an institutional investor for more than its surrender value but less than the death benefit. In exchange, the policyholder receives a lump sum of cash, which can be used immediately for expenses such as senior home care services or elder care. The buyer then takes over premium payments and collects the death benefit when the policy matures.

Even though term life policies generally have no built-in cash value, many can still qualify for a life settlement if they are convertible or if there is investor interest based on the insured’s age, health, and policy size.

When a Viatical Settlement May Apply

In some cases, a policyholder requiring home care for seniors may qualify for a viatical settlement, which is similar to a life settlement, but is designed specifically for individuals with a life expectancy of 24 months or less due to serious illness. Viatical settlements typically provide higher payouts than standard life settlements because the investor’s return is realized sooner. These funds can be critical for covering senior care at home, medical equipment, or specialized treatments that improve quality of life. Viatical settlement proceeds are generally tax free, but of course it is always important to consult with your trusted tax advisor based on your unique situation.

Who Is Eligible?

Eligibility depends on a few main factors:

- The insured is usually age 65 or older (younger with significant health conditions)

- The policy has a death benefit of at least $100,000.

- The policy is active and in good standing.

- The terms of the policy make it attractive to buyers (convertible term policies often qualify)

If these conditions are met, the policyholder may be able to receive a cash payout based on the hidden value in their policy.

Benefits of Using a Life or Viatical Settlement for Care

Selling a policy can ease financial strain at a critical time, helping cover the cost of home care assistance, elderly home care, or other supportive services. Key benefits include:

- Immediate cash: Funds are usually available within weeks.

- Flexibility: Money can be used for home care services, medications, or other personal needs.

- Better value: Settlements often yield more than surrendering or abandoning the policy, especially in the case of term insurance policies.

- Family support: Relieves loved ones of the pressure to cover home care for elderly family members.

Important Considerations

Selling a term life insurance policy is a significant financial decision. While the cash payout can help cover the high cost of senior home care, there are a few important points to think through carefully:

- Taxes: Depending on your situation, part of the payout may be taxable. It’s wise to understand how this could affect your overall finances.

- Impact on beneficiaries: Once a policy is sold, the original death benefit will no longer go to family members or heirs. This trade-off should be weighed against the immediate need for funds.

- Future financial planning: Consider how selling the policy fits into your broader financial goals. For some, accessing cash today brings peace of mind and stability; for others, keeping coverage in place may still serve a purpose.

By weighing these factors, individuals can make an informed choice that best fits their care needs and long-term priorities.

A Path Toward Security at Home

Paying for in home care services with term life insurance may not be the first option families consider, but it can be a valuable option. Life settlements and viatical settlements give policyholders a chance to use their coverage while they are still alive, transforming an expiring policy into a source of financial stability.

By exploring these options, families can make informed decisions that protect dignity, provide comfort, and ensure that quality senior home care services remain within reach.

To learn if you or your loved one qualify to access the hidden value in an existing life insurance policy, please reach out to us at 800-973-8258. In a short 5-10 minute call, we can help you learn if your term life insurance policy may be a viable option for in home care funding.