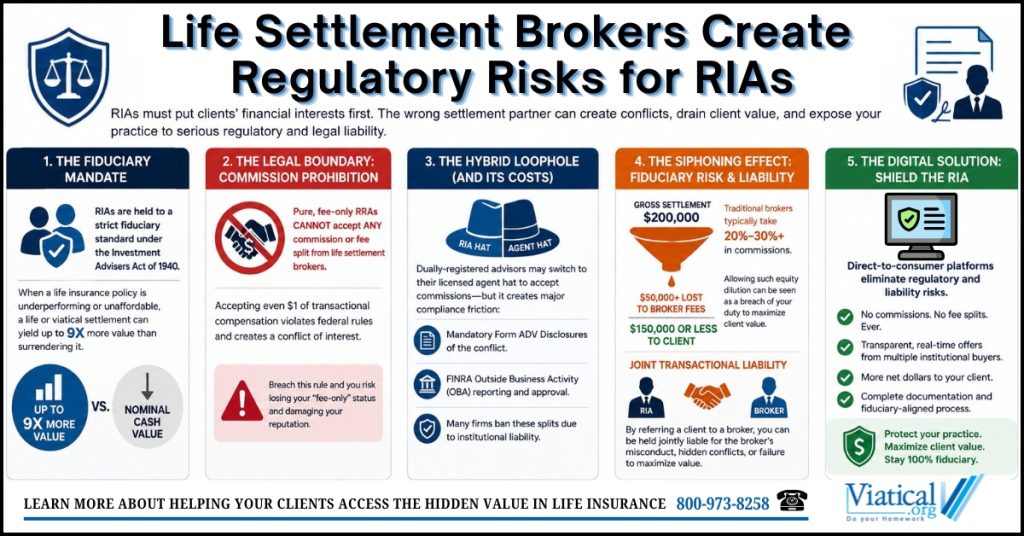

Registered Investment Advisors (RIAs) operate under a strict, non-negotiable federal fiduciary standard mandated by the Investment Advisers Act of 1940. This legal framework requires advisors to place their clients’ financial interests above all else, ensuring complete transparency, minimizing transactional conflicts, and seeking the highest possible net yield for a client’s assets.

When a senior or chronically ill client holds an underperforming or unaffordable life insurance policy, an ethical RIA naturally looks to the secondary market for a solution. Liquidating a policy via life settlements or a viatical settlement can yield up to nine times more value than surrendering it back to the carrier for nominal cash value.

However, the transactional mechanism an advisor selects to execute this settlement can unintentionally trigger severe regulatory violations, compromise their fiduciary purity, and expose their practice to devastating legal liability.

Why Pure RIAs Cannot Touch Broker Commissions

The most immediate regulatory hurdle for a pure, fee-only RIA is the absolute prohibition against transaction-based compensation. Traditional secondary market transactions are dominated by life settlement brokers who operate entirely on a commission-based framework.

The “Fee-Only” Marketing Violation

If an RIA firm markets itself as a “fee-only” fiduciary practice, meaning it charges strictly via an Assets Under Management (AUM) percentage, flat financial planning retainers, or hourly fees, it is completely barred from accepting any portion of an insurance commission or broker fee-split.

Accepting even a single dollar of transactional compensation from a traditional life settlement broker instantly violates federal compliance guidelines. The Securities and Exchange Commission (SEC) and state regulators view the receipt of a transaction-based commission as a direct conflict of interest, as it incentivizes the advisor to recommend a specific transaction for personal enrichment rather than the client’s sole benefit. Furthermore, regulatory bodies and professional standard boards, such as the CFP Board, will aggressively strip “fee-only” designations from advisors who breach this rule, severely damaging the firm’s public reputation.

The Hybrid Advisory Loophole and Its Regulatory Costs

To bypass this restriction, many financial professionals utilize a dually-registered “hybrid” RIA model. Under this dual structure, the professional operates an independent RIA for wealth management but maintains an active registration with an affiliated Broker-Dealer or holds an independent Life and Health Insurance License.

When a life settlement arises, the advisor attempts to remove their “RIA hat” and put on their “licensed agent hat” to accept a commission split from a life settlement broker. While technically legal, this approach introduces a mountain of compliance friction:

- Mandatory Form ADV Disclosures: The advisor must explicitly document this capacity in Form ADV Part 2A, detailing the conflict of interest in written text to the client.

- FINRA Outside Business Activity (OBA) Rules: The transaction must be reported and approved by the advisor’s broker-dealer as an Outside Business Activity or a Private Securities Transaction.

- Corporate Prohibitions: Because the secondary life insurance market has historically been plagued by opaque pricing, many conservative corporate compliance departments outright ban these splits due to the severe institutional liability they create.

How Traditional Brokers Violate Fiduciary Duty

Even if an RIA does not accept a dime of the commission, routing a fiduciary client to a traditional life settlement broker creates an inherent structural conflict. Traditional brokers handle client transactions by shopping a policy across multiple institutional buyers, but they extract an immense financial toll for doing so.

Historically, traditional life settlement brokers charge commissions ranging from 20% to 30% or more of the total settlement value. For example, if a broker secures a gross market value of $200,000 for a terminally ill client’s policy, they may siphon off $50,000 or more to cover their internal transactional fees and intermediary markups.

Under the fiduciary standard, an advisor has an ongoing obligation to protect the client’s asset equity. If an RIA facilitates a transaction where a third-party intermediary slices off a massive percentage of the client’s net payout, the advisor must be prepared to legally justify why they permitted such extreme equity dilution when more efficient market alternatives existed.

Joint Transactional Liability

Most independent investment advisors erroneously believe that because they lack specialized knowledge of the secondary market, they cannot be held responsible for a broker’s down-market conduct. In a court of law, this defense fails under standard agency law.

When an RIA introduces a broker to a client to execute a settlement, the broker is a fiduciary by statute in nearly every regulated state. By participating in a single, joint transaction, the RIA effectively hitches their professional liability to that broker. If the broker engages in uncompetitive bidding pools, acts with hidden conflicts, or fails to maximize the transaction value, the client’s estate can sue both the broker and the referring advisor for a negligent referral and a breach of the duty of care.

How Direct-to-Consumer Platforms Shield the RIA

To completely eliminate the regulatory gridlock and liability risks associated with traditional brokers, forward-thinking RIAs are shifting entirely to independent, open-architecture direct-to-consumer platforms. Pioneered by direct models like Viatical.org, which introduced this framework to the Life Insurance Settlement Association (LISA) in 2016, the direct-to-consumer infrastructure completely rewrites the compliance playbook.

1. Eliminating Consumer-Side Commissions ($0.00 Cost)

A true direct-to-consumer platform bypasses traditional broker disclosure regulations by removing the consumer-side fee from the mathematical equation entirely. Instead of deducting a percentage from the client’s payout, the platform charges 0% in consumer-side commissions.

The operational costs of managing secure medical records, running carrier policy illustrations, and maintaining the digital interface are monetized on the backend. The platform passes these overhead expenses onto the purchasing institutional funds as a flat technology access fee. For the RIA’s client, the gross offer made by the institutional buyer is the exact net amount they receive at closing.

2. Safeguarding Fiduciary Purity and Capital Growth

By utilizing a direct platform, a pure fee-only RIA completely preserves its regulatory status. There is no commission pool to split, completely removing any temptation or allegation of self-dealing.

More importantly, it maximizes the client’s investable capital. Rather than losing $50,000 of asset value to an intermediary broker, that equity is paid fully to the elderly or terminally ill client. Those un-diluted settlement proceeds can then be cleanly deposited directly into the client’s managed investment accounts. This allows the RIA to ethically and legally increase their standard AUM advisory fees while ensuring the client retains the true market value of their liquidated asset.

3. De-Risking the Wealth Management Practice

Direct platforms utilize specific compliance protections designed to legally insulate referring professionals:

- The Multi-Buyer Automated Clearinghouse: The platform automatically distributes anonymized policy data to all qualified, state-licensed institutional buyers simultaneously. This competitive digital auction provides the RIA with a mathematically verifiable defense that true market value was achieved on an open exchange.

- Bipartite HIPAA Data-Vaults: Clients upload their highly sensitive medical documentation directly into an encrypted, HIPAA-compliant platform. Because the records bypass the advisor’s local corporate network entirely, the RIA is completely insulated from data-breach and privacy-law liability.

A Compliance Imperative for Modern Fiduciaries

The regulatory landscape governing secondary market insurance transactions is tightening. Recent judicial precedents make it clear that financial professionals face severe exposure if they ignore a client’s distressed life insurance policies, or if they blindly route clients to inefficient, high-fee traditional broker networks.

For Registered Investment Advisors, the choice is clear. Relying on traditional life settlement brokers introduces severe structural conflicts, creates joint liability traps, and unnecessarily strips away up to 30% of a client’s personal wealth. By transitioning to a true direct-to-consumer digital clearinghouse model, RIAs can flawlessly uphold their fiduciary mandates, insulate their practices from regulatory scrutiny, and guarantee that their clients walk away from the closing table with the maximum possible payout.

To learn more about helping your clients access the hidden value in life insurance, please give us a call at 800-973-8258.