Receiving a notice that your life insurance policy is about to lapse can be stressful, especially if the premiums have become difficult to afford. At that point many people begin searching for answers, including the question: can you sell a life insurance policy that is about to lapse? In many cases, the answer may be yes. If the policy is still active and meets certain criteria, it may be possible to sell it in the secondary market rather than letting it expire with no value.

Understanding how timing works is important because once a policy actually lapses, the opportunity to sell it may disappear.

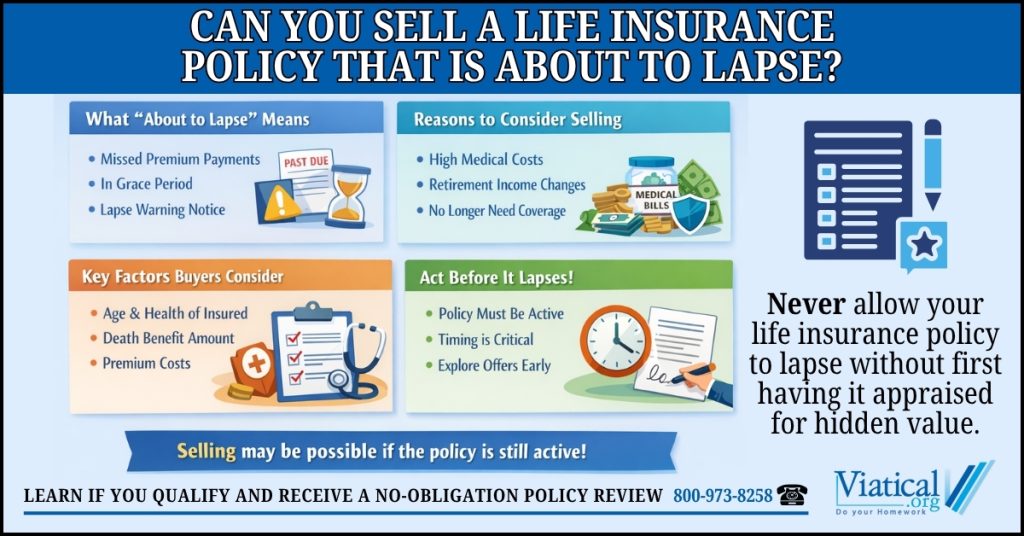

What It Means When a Policy Is About to Lapse

A life insurance policy is considered “about to lapse” when the required premium has not been paid and the policy is approaching the end of its grace period. Most policies include a grace period that lasts about 30 to 60 days.

During this time:

- Coverage typically remains in force

- The insurer sends notices requesting payment

- The policyowner still has an opportunity to bring the policy current

If the premium is not paid before the grace period ends, the policy usually terminates.

From a life settlement standpoint, the key point is that the policy generally must still be active in order to be sold.

Why Some Policyowners Consider Selling Instead of Letting a Policy Lapse

When a policyowner can no longer afford premiums, allowing the policy to lapse may seem like the simplest option. Unfortunately, that often means walking away from something that may have real value.

A life settlement may allow you to receive a lump-sum cash payment instead of letting the policy expire with no benefit.

Common reasons people explore this option include:

- Retirement income changes that make premiums difficult to maintain

- Medical expenses or long-term care costs

- Policies purchased decades earlier that are no longer needed for family protection

- Policies that have become too expensive after premium increases

Even when a policy has little or no cash value, it may still qualify for a life settlement if the insured meets certain age or health criteria.

How Buyers Evaluate Policies That Are Near Lapse

Settlement purchasers review several factors when determining whether a policy may qualify for purchase, including:

- Age of the insured

- Health status and medical history

- Size of the death benefit

- Premium obligations

- Policy type and structure

If a policy is about to lapse, timing becomes particularly important because buyers typically need the policy to remain active while underwriting is completed.

In some cases, a buyer may move quickly if the policy meets typical settlement guidelines. In other situations, the policyowner may need to pay a premium to keep the policy active during the evaluation process.

Acting Before the Policy Actually Lapses

Once a policy fully lapses, selling it usually becomes much more difficult. Some policies may be eligible for reinstatement after lapse, but that process often requires new medical information and payment of past premiums.

For this reason, policyowners who believe they may stop paying premiums often benefit from exploring their options before the policy terminates.

Taking action early may allow enough time for:

- Policy review and eligibility evaluation

- Medical underwriting

- Settlement offers from potential buyers

Waiting until the final days of the grace period can make the process much more challenging.

A Possible Alternative to Losing the Policy Entirely

Life insurance policies are legally recognized financial assets. Just like other assets, they may sometimes be sold rather than abandoned.

For policyowners asking can you sell a life insurance policy that is about to lapse, the answer is often yes, as long as the policy is still active and meets buyer guidelines. Exploring a life settlement before the policy expires may provide a way to recover value that would otherwise be lost if coverage simply ends.

To learn if you’re likely to qualify for life settlements or a viatical settlement to access your policy’s hidden value before it lapses, please give us a call at 800-973-8258.