Many policyholders wonder: can you sell a life insurance policy without cash value? The short answer is yes, in many cases you can. While traditional wisdom suggests that only permanent life insurance with an accumulated cash value can be sold, the secondary market offers solutions for certain term policies and other policies that have little or no cash value at all. Understanding how this works can help you determine whether selling your policy is a viable option for accessing funds when you need them most.

Understanding Cash Value vs. Market Value

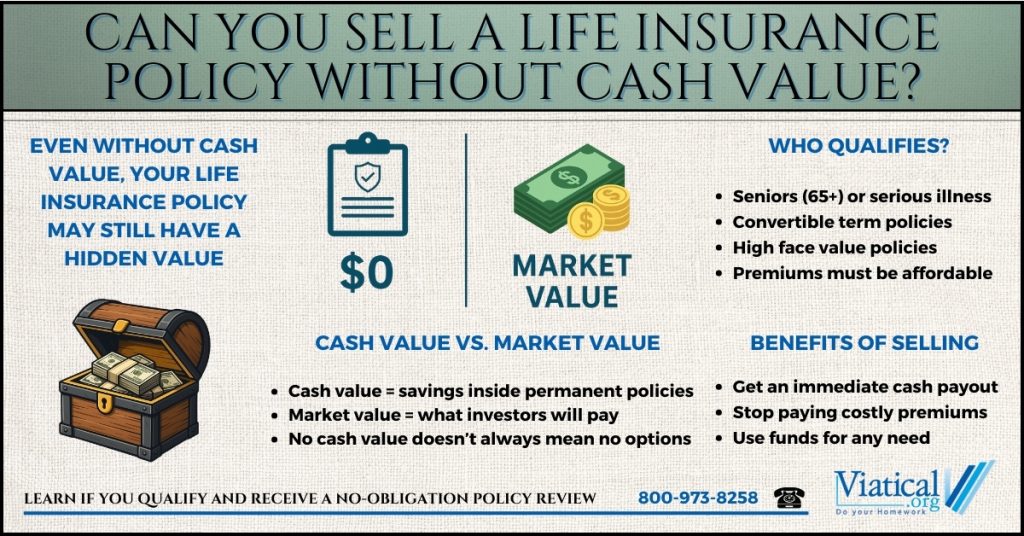

Cash value is the savings component of certain permanent life insurance policies, such as whole life or universal life. It grows over time and can be borrowed against or surrendered back to the insurance company.

However, secondary market value is different. Even if your policy doesn’t have cash value, it may still have market value to an investor. In life settlements or viatical settlement, investors purchase the policy, take over premium payments, and eventually collect the death benefit. This creates an opportunity for policyholders who otherwise might let a policy lapse or surrender it for little or nothing.

Selling Term Life Insurance

Term life policies typically do not build cash value, which often leads people to assume they can’t be sold. But under the right circumstances, you can sell your life insurance policy for cash:

- Convertible Term Policies: Many term policies have a conversion feature that allows the policyholder to convert to a permanent policy without undergoing new medical underwriting. Once converted, the policy becomes eligible for sale.

- High Face Value Policies: Policies with significant death benefits and insureds with health impairments are often attractive to buyers, even if there is no cash value.

Who Qualifies to Sell a Policy Without Cash Value?

Eligibility depends on several factors beyond just whether a policy has accumulated value:

- Age and Health: Generally, insureds over age 65 or those with a serious or terminal illness are the strongest candidates.

- Policy Type: Universal life, whole life, and convertible term policies are most commonly sold. But even group policies or non-convertible term policies may sometimes qualify.

- Premium Costs: The affordability of ongoing premiums plays a role in determining whether investors are willing to purchase the policy.

Benefits of Selling a No-Cash-Value Policy

If your policy qualifies, selling can provide several important benefits:

- Access to Immediate Funds: Rather than letting your policy lapse, you can receive a lump sum payment.

- Higher Payout than Surrender Value: Even policies with zero cash surrender value can generate thousands of dollars in the settlement market.

- Relief from Premium Payments: Once sold, you are no longer responsible for paying costly premiums.

- Flexibility: Proceeds can be used for medical costs, debt repayment, retirement, or any other financial need.

The Settlement Process

If you’re considering selling, here’s what typically happens:

- Policy Review: Prospective buyers evaluate your policy details, premiums, and your health profile/medical records.

- Offer: If value is found and there is interest, a direct buyer will present an offer to you.

- Sale Agreement: If you accept an offer, contracts are signed and ownership and beneficiary rights are transferred to the buyer.

- Payment: You receive a lump sum, and the buyer assumes responsibility for all future premiums.

So, can you sell a life insurance policy without cash value? Yes, under the right circumstances you can receive a cash payout for life insurance. Even term policies with no built-in savings can sometimes be sold for a significant amount, providing policyholders with financial relief that would otherwise be lost. If you own a life insurance policy you no longer need or can no longer afford, exploring the secondary market could reveal hidden value where you least expect it.

To learn if you qualify and obtain a no-obligation policy appraisal, please give us a call at 800-973-8258.