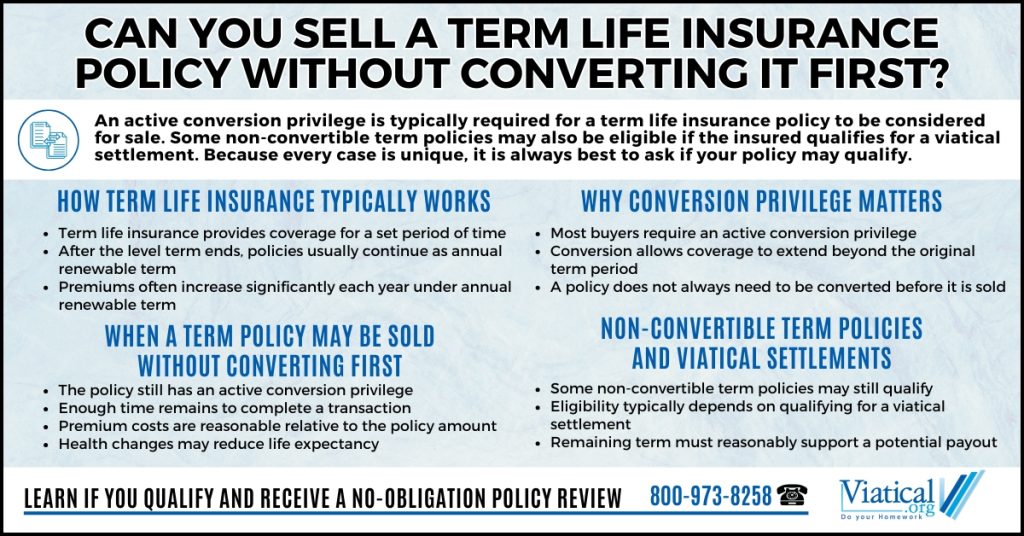

Can you sell a term life insurance policy without converting it first? Yes, you may be able to sell term life insurance without converting it first, but most buyers require that the policy still has an active conversion privilege. In many cases, the conversion option is what makes a term policy eligible for purchase, even if the policy is not converted before the sale. However, there are limited situations where a non-convertible term policy may still qualify, particularly when the insured meets viatical settlement criteria.

Why Conversion Privilege Usually Matters

Most term life insurance policies do not simply end at the conclusion of the level term period. Instead, they typically continue as annual renewable term, allowing the policy to remain in force while premiums increase each year, often significantly.

From a buyer’s perspective, annual renewable term introduces uncertainty. Premiums can rise quickly, sometimes making the policy prohibitively expensive to maintain. An active conversion privilege helps address this risk by providing a way to convert the policy to permanent coverage if needed, allowing coverage to continue under a more predictable premium structure.

Because of this, most buyers require that a term policy still be convertible, even if conversion is not completed at the time of sale.

When You May Be Able to Sell Without Converting First

You generally do not need to convert your term policy before exploring offers if the policy has:

- An active conversion privilege that has not expired

- Enough remaining level term or conversion time to complete underwriting and closing

- A face amount large enough to justify ongoing premiums

- Health changes that materially reduce life expectancy

In these situations, a buyer may purchase the policy while it remains term coverage and decide later whether conversion is necessary.

Non-Convertible Term Policies and Viatical Settlements

While most term policies must be convertible to qualify, some non-convertible term policies may still be eligible in viatical settlement cases, depending on health and timing.

If an individual qualifies for a viatical settlement, typically meaning a life expectancy of two years or less, a buyer may be willing to purchase a non-convertible term policy if the remaining term is sufficient to reasonably expect a payout before the policy becomes unaffordable or reaches the end of coverage.

These cases are less common and highly dependent on the specifics. Remaining term length, premium schedule, policy size, and medical documentation all matter. Because of this, each case is different and it is always best to ask, even when a policy does not appear to qualify at first glance.

When Annual Renewable Term Becomes a Limiting Factor

Even when a policy can continue as annual renewable term, buyers may hesitate if:

- Premiums increase sharply year over year

- The policy becomes financially inefficient relative to the death benefit

- The remaining term does not align with the insured’s medical outlook

A policy may technically stay in force, but escalating premiums can make it impractical for a buyer to maintain.

What Buyers Typically Review

When evaluating a term life insurance policy, buyers usually examine:

- Carrier, face amount, and current premium

- Remaining level term and annual renewable term schedule

- Conversion availability and deadlines, if applicable

- Medical records and projected life expectancy

How To Decide Whether Selling Is an Option

Whether a term life insurance policy can be sold without converting it first depends on several factors, including conversion status, remaining term, premium structure, and health. While most buyers require an active conversion privilege, some non-convertible term policies may still qualify in viatical settlement situations. Because eligibility is highly case-specific, reviewing the policy before allowing it to lapse or assuming it has no value can help determine whether selling is an option.

It is always best to explore a sale at least 6 months prior to the end of your conversion privilege. To learn if you’re likely to qualify to sell your term life insurance policy for cash, please give us a call today. 800-973-8258