Typically, the first thing our callers want to know is if their health qualifies them for a viatical settlement. The simple answer to our most common question ‘How sick do I have to be for a viatical settlement?’ is that you must have a life expectancy of less than 2 years. But that simply has to do with how your payment from your viatical settlement would be treated federally for taxation purposes, rather than if you qualify of not to sell your life insurance policy. Your overall health and specific diagnosis ultimately drive any value your life insurance policy may have as a viatical settlement, but the type and amount of insurance you have is a major factor as well.

Over the past 20 years, we have tried to help people who were terminally ill sell their insurance policy and simply couldn’t because of various provisions or restrictions and we’ve helped other people successfully sell their insurance policy when they were in perfect health and with a life expectancy of over 20 years. Each case is unique.

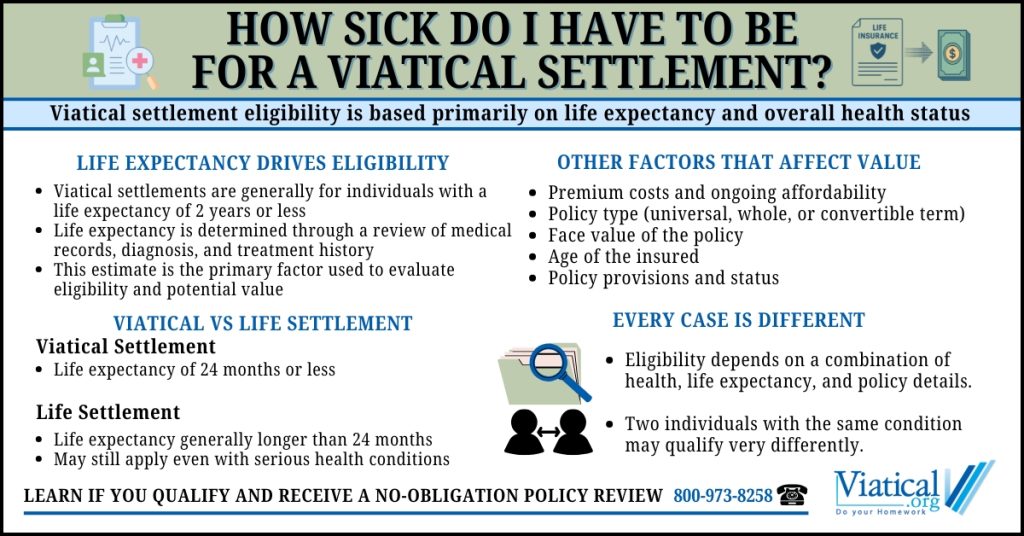

The Role of Life Expectancy

The most important factor in a viatical settlement is projected life expectancy. By definition, viatical settlements are not taxed and considered an accelerated payment of your death benefit provided you are terminally ill of chronically ill with some provisions. This standard is built into state regulations and industry guidelines.

Life expectancy is determined through a formal underwriting process that evaluates:

- Medical records and physician statements

- Diagnosis and stage of illness

- Treatment history and response

- Prescription data and related conditions

- Actuarial life tables and underwriting models

Medical underwriters use this information to estimate how long an individual is likely to live. This estimate directly impacts both your eligibility and your offer. Some buyers do their own internal underwriting, but most buyers utilize third party Life Expectancy Providers to meet the standards of their respective funds and many institutional buyers of life insurance policies require two life expectancy reports.

If a person has a serious or even terminal condition but their life expectancy exceeds two years, you still could qualify to sell your policy, but the policy may not qualify as a viatical settlement. Instead, it may qualify as a life settlement.

- Viatical settlement: Typically requires a life expectancy of 24 months or less

- Life settlement: Often applies to longer life expectancies, even with serious health conditions

This distinction between viatical vs life settlements affects both eligibility and the expected payout.

Viatical Settlement Examples

The following examples show how policy type, life expectancy, and health condition work together:

Example 1: Advanced Cancer (Viatical Settlement)

- Policy Type: Universal life

- Face Value: $500,000

- Age: 67

- Condition: Late-stage pancreatic cancer, no longer responding to treatment

- Life Expectancy: 9–14 months

- Payout: $340,000

Example 2: ALS Progression (Viatical Settlement)

- Policy Type: Term life (converted to permanent)

- Face Value: $250,000

- Age: 60

- Condition: Amyotrophic Lateral Sclerosis with rapid respiratory decline

- Life Expectancy: 18–24 months

- Payout: $165,000

Example 3: Severe Congestive Heart Failure (Viatical Settlement)

- Policy Type: Whole life

- Face Value: $150,000

- Age: 74

- Condition: Advanced heart failure with repeated hospitalizations

- Life Expectancy: 12–18 months

- Payout: $90,000

Example 4: Cancer with Extended Prognosis (Life Settlement)

- Policy Type: Universal life

- Face Value: $400,000

- Age: 66

- Condition: Cancer responding to treatment

- Life Expectancy: 5–7 years

- Payout: $85,000

Example 5: Chronic Condition with Long-Term Outlook (Life Settlement)

- Policy Type: Term life

- Face Value: $300,000

- Age: 70

- Condition: Diabetes with complications but stable management

- Life Expectancy: 8–10+ years

- Payout: $45,000

Each Case is Unique

Even when two individuals have the same diagnosis, their eligibility can vary significantly. Life expectancy depends on disease progression, treatment response, and overall health.

Because of this, there is no universal rule beyond the general two-year guideline. Some cases clearly qualify for a viatical settlement, while others fall into the life settlement category.

In addition to life expectancy, several policy and financial factors can also affect whether a policy qualifies and how much it may be worth, including:

- Premium costs and whether they are manageable relative to the policy size

- Type of policy (universal life, whole life, or convertible term)

- Face value of the policy

- Age of the insured

- Policy provisions, such as conversion options or whether the contestability period has passed

- Insurance company strength

Your premiums are especially important. Policies with lower ongoing costs are generally more attractive because they require less out-of-pocket expense to keep in force. Higher premiums will reduce the amount a policyowner may receive, even when the life expectancy meets viatical guidelines.

The most accurate way to understand where you stand is to have your specific situation reviewed based specifically on your health and your policy. You can easily learn if you’re likely to qualify with a brief 5-10 minute phone call. 800-973-8258 No question is too small.

Frequently Asked Questions

Do I need to be terminally ill to qualify?

In most cases yes. If someone is 104 years old with a natural life expectancy of less than 2 years would be an exception. Viatical settlements are intended for individuals with a life expectancy of two years or less.

Who determines life expectancy?

Independent Life Expectancy (LE) medical underwriters evaluate your medical records, diagnosis, and treatment history.

Can I qualify if I am still receiving treatment?

Yes. Ongoing treatment does not prevent qualification for a viatical if your life expectancy meets the viatical guidelines.

What if my life expectancy is longer than two years?

You may still qualify for life settlements instead of a viatical settlement if your life expectancy exceeds two years.

Do different policy types affect eligibility?

Yes. Majorly. Universal life, whole life, and convertible term policies are commonly eligible, but each case is evaluated individually. Group Life Insurance and non-convertible annual renewable term insurance may be sold, but you have to be terminally ill because of the exponential premiums.

Does payout depend on how sick I am?

Yes. Your payout is primarily based on your life expectancy or how sick you are. Shorter life expectancies typically result in higher offers relative to the policy’s face value.