For decades, individuals looking to sell their life insurance policies through a viatical or life settlement faced a system built around intermediaries rather than through direct to consumer viatical settlements. Brokers, providers, and institutional buyers all played a role, but at a cost. By the time a transaction closed, policyholders often received only a fraction of what their policy was actually worth in the secondary market.

That began to change in 2016 when Viatical.org introduced a direct to consumer model to the Life Insurance Settlement Association (LISA). This approach challenged the traditional structure and put more control (and more money) back into the hands of policyowners.

Today, direct to consumer viatical settlements are reshaping the industry, offering transparency, efficiency, and significantly improved financial outcomes for sellers.

Understanding Traditional Viatical and Life Settlement Models

Before diving into the benefits of the direct to consumer approach, it’s important to understand how the traditional model worked.

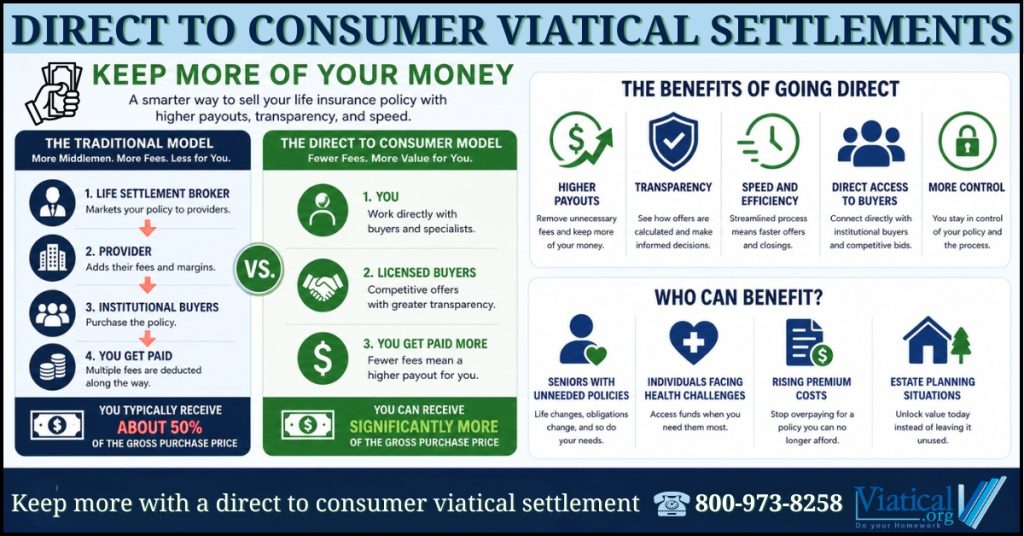

Historically, if you wanted to sell your life insurance policy, you would:

- Contact a life settlement broker

- The broker would market your policy to multiple providers

- Providers would present offers from institutional buyers

- Fees would be deducted at multiple levels before you received your payout

These fees typically included:

- Broker commissions (often 15% to 30% or more)

- Provider fees and margins

- Administrative and transactional costs

By the end of the process, many policyholders received only about 50% of the gross purchase price paid by the institutional fund acquiring the policy.

The Problem: Hidden Costs and Lack of Transparency

One of the biggest challenges with the traditional model is that most sellers never see the full economics of their transaction.

Key issues include:

- Opaque pricing structures

- Layered fees that are not clearly disclosed

- Misaligned incentives between brokers and sellers

- Limited control over the process

In many cases, sellers assume they are getting the best possible offer without realizing how much is being taken out before the funds reach them.

This lack of transparency has historically made it difficult for policyholders to make fully informed decisions.

What Is a Direct to Consumer Viatical Settlement?

A direct to consumer viatical settlement eliminates unnecessary intermediaries by allowing policyholders to work directly with a platform or buyer network.

Instead of relying on a broker to manage the transaction, the policyholder engages directly with:

- Licensed buyers or funding sources

- Underwriting professionals

- Settlement specialists

This streamlined model reduces friction and removes multiple layers of fees.

How Viatical.org Changed the Industry in 2016

In 2016, Viatical.org introduced the direct to consumer concept to LISA, marking a significant turning point in how life settlements could be structured.

Rather than accepting the status quo, this model proposed:

- Direct engagement between policyholders and buyers

- Greater transparency in pricing and offers

- Reduced dependency on traditional broker networks

The result was a shift toward a more consumer focused system where sellers could finally understand the true value of their policies and retain a much larger portion of the proceeds.

Why Direct to Consumer Means Higher Payouts

The most compelling advantage of the direct to consumer model is simple: you keep more of your money.

By removing or reducing broker involvement:

- Fewer commissions are deducted

- Pricing becomes more competitive

- Buyers can offer stronger net payouts

In many cases, policyholders can receive significantly more than the traditional 50% average of the gross purchase price.

This difference can amount to tens or even hundreds of thousands of dollars depending on the size of the policy.

Transparency: Knowing What Your Policy Is Really Worth

Direct-to-consumer viatical settlements also introduce a level of transparency that has historically been missing from the industry.

With fewer intermediaries, sellers can:

- See how offers are calculated

- Understand underwriting assumptions

- Compare multiple bids more clearly

- Make informed decisions without hidden agendas

Transparency builds trust and trust leads to better outcomes for everyone involved.

Speed and Efficiency in the Process

Another major benefit is speed.

Traditional brokered transactions can take months due to:

- Back and forth negotiations

- Multiple approval layers

- Complex communication chains

Direct to consumer models streamline this by:

- Reducing decision-makers

- Simplifying documentation

- Accelerating underwriting and offer generation

For individuals facing urgent financial or medical needs, this faster timeline can be critical.

Who Benefits Most from Direct to Consumer Viaticals?

While nearly any policyholder can benefit, certain groups stand to gain the most:

1. Seniors with Unneeded Policies

Many older individuals no longer need their life insurance due to:

- Changed financial circumstances

- Paid-off obligations

- Estate planning shifts

2. Individuals Facing Health Challenges

Those with serious or chronic health conditions may qualify for viatical settlements and need immediate liquidity.

3. Policyholders with Rising Premium Costs

When premiums become unaffordable, selling the policy can be far better than lapsing it for no value.

4. Estate Planning Situations

Direct sales can unlock value that would otherwise remain inaccessible.

Direct Access to Institutional Buyers

One misconception is that removing brokers limits access to buyers. In reality, the opposite is often true.

Direct to consumer platforms can:

- Connect policyholders directly with institutional funds

- Facilitate competitive bidding environments

- Ensure that offers reflect true market demand

This direct access helps ensure that sellers are not leaving money on the table.

Compliance and Consumer Protection

A well-structured direct to consumer model still adheres to all regulatory requirements, including:

- State licensing laws

- Disclosure obligations

- Privacy protections (including HIPAA compliance where applicable)

In fact, transparency often enhances compliance by making all aspects of the transaction clearer to the seller.

Common Myths About Cutting Out the Broker

Myth 1: Brokers Always Get Better Offers

Reality: Offers are driven by institutional buyers, not brokers. Direct access can produce equally strong or better bids.

Myth 2: The Process Is Too Complex Without a Broker

Reality: Modern platforms simplify the process and guide sellers step by step.

Myth 3: You Lose Protection Without a Broker

Reality: Properly structured direct models maintain full regulatory compliance and consumer safeguards.

The Future of Life Settlements Is Direct

The financial services industry is evolving across the board toward direct to consumer models:

- Investing (self-directed platforms)

- Insurance (online underwriting and policy management)

- Lending (direct marketplaces)

Life settlements are no exception.

As awareness grows, more policyholders are recognizing that they have options and that those options don’t have to include giving up a large percentage of their policy’s value.

Why This Matters More Than Ever

Millions of Americans own life insurance policies they no longer need or can no longer afford. Historically, many of these policies:

- Lapse with zero value

- Are surrendered for minimal cash

- Or are sold with excessive fees

Direct to consumer viatical settlements provide a third path, one that maximizes value while maintaining control.

Taking Control of Your Financial Asset

Your life insurance policy is more than just a safety net – it’s a financial asset.

Like any asset, it should be:

- Evaluated

- Priced competitively

- Sold in a way that maximizes return

The direct to consumer model empowers you to do exactly that.

A Smarter Way to Sell Your Policy

The introduction of direct to consumer viatical settlements in 2016 marked a turning point in the industry. By challenging traditional broker-dominated structures, Viatical.org helped open the door to a more transparent, efficient, and consumer-friendly approach.

If you’re considering selling your life insurance policy, the question is no longer just whether to sell, but how.

And increasingly, the answer is clear: Go direct. Keep more. Stay in control.

To learn if you qualify to access your policy’s hidden value, please give us a call at 800-973-8258