Facing a serious medical diagnosis often brings immediate financial questions, especially when income drops and medical expenses rise. Life insurance options after a life-changing diagnosis are not always explained by doctors or insurance companies, yet they can provide financial flexibility during a difficult time. Many people assume their life insurance policy is something that only helps others in the future, but in some cases, it may offer options that can be used while the policyholder is still living.

A life-changing diagnosis may involve advanced cancer, progressive neurological conditions, heart disease, organ failure, or other illnesses that significantly affect daily functioning or long-term health outlook. As health declines, financial priorities often shift from long-term planning to managing immediate needs such as treatment costs, home care, transportation, or basic living expenses. Understanding how an existing life insurance policy fits into that situation can help prevent missed opportunities.

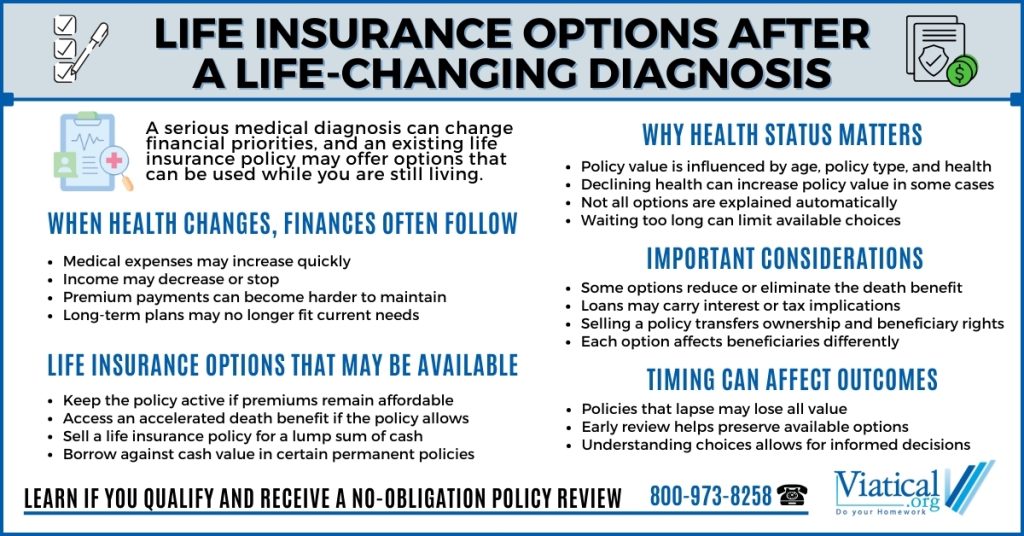

Keeping the Policy in Force

Some individuals choose to continue paying premiums, especially if beneficiaries still depend on the future death benefit. This approach may make sense when premiums remain affordable and household finances are stable. However, serious illness often changes that balance. Medical bills, reduced work hours, or the inability to work at all can make ongoing premium payments difficult.

If a policy lapses due to nonpayment, any potential value tied to that policy may be lost. Reviewing available alternatives before reaching that point can help preserve options that might otherwise disappear.

Accelerated Death Benefit Options

Many life insurance policies include an accelerated death benefit rider. This feature may allow individuals with qualifying medical conditions to receive a portion of the death benefit early. The funds are typically unrestricted and can be used for medical costs, living expenses, or other financial needs.

Eligibility requirements and payout limits vary by policy. Accessing accelerated benefits reduces the remaining death benefit available to beneficiaries, which is an important consideration for families who rely on that future payout.

Selling a Life Insurance Policy

For individuals whose health has declined significantly, selling a life insurance policy through a viatical settlement or life settlements may be an option. In this arrangement, a buyer purchases the policy, assumes responsibility for future premium payments, and becomes the beneficiary. The policyholder receives a lump sum cash payment while still living.

The amount offered depends on several factors, including age, policy type, death benefit amount, and medical condition. In many cases, declining health can increase the potential value of a policy in the secondary market, since the expected duration of future premium payments may be shorter. This is often unexpected for policyholders who assume that poor health limits their choices.

Accessing Cash Value or Policy Loans

Permanent life insurance policies may allow policyholders to borrow against or withdraw from accumulated cash value. While this can provide short-term liquidity, it typically reduces the death benefit and may result in interest charges or tax consequences.

For individuals dealing with serious illness, loans may offer limited relief if repayment is not realistic. In some situations, borrowing against a policy can complicate future options rather than improve financial stability.

Comparing the Tradeoffs

Each life insurance option comes with different consequences. An accelerated benefit and loans reduce the eventual payout to beneficiaries. Selling a policy eliminates the death benefit but can provide immediate funds without repayment obligations.

The right choice depends on personal financial needs, family responsibilities, and health circumstances. What matters most is recognizing that a life insurance policy can function as a financial asset, not just a future benefit. Allowing a policy to lapse or surrendering it without exploring alternatives may result in lost value.

Acting Before Options Narrow

Timing is an important factor after a life-changing diagnosis. Once premiums become unaffordable or a policy is canceled, available choices may be limited. Reviewing policy details early and understanding the available paths can help protect access to funds when they are most needed.

Life insurance decisions are rarely easy during periods of illness. Having clear information about life insurance options after a life-changing diagnosis can help individuals and families make informed financial decisions during an already challenging time.

To learn more about your options, please give us a call at 800-973-8258. It typically only takes a 5-10 minute phone call to learn if you qualify to access the hidden value in your life insurance policy.