What makes a life insurance policy attractive to buyers? This is one of the most common questions policyholders ask when they are considering whether selling their life insurance policy is an option. Not all policies qualify, and not all qualifying policies are valued the same way. Buyers evaluate several specific factors to determine whether a policy has market value and how much they may be willing to pay for it.

Understanding these factors can help you decide whether it makes sense to explore selling your policy rather than letting it lapse or surrendering it back to the insurance company.

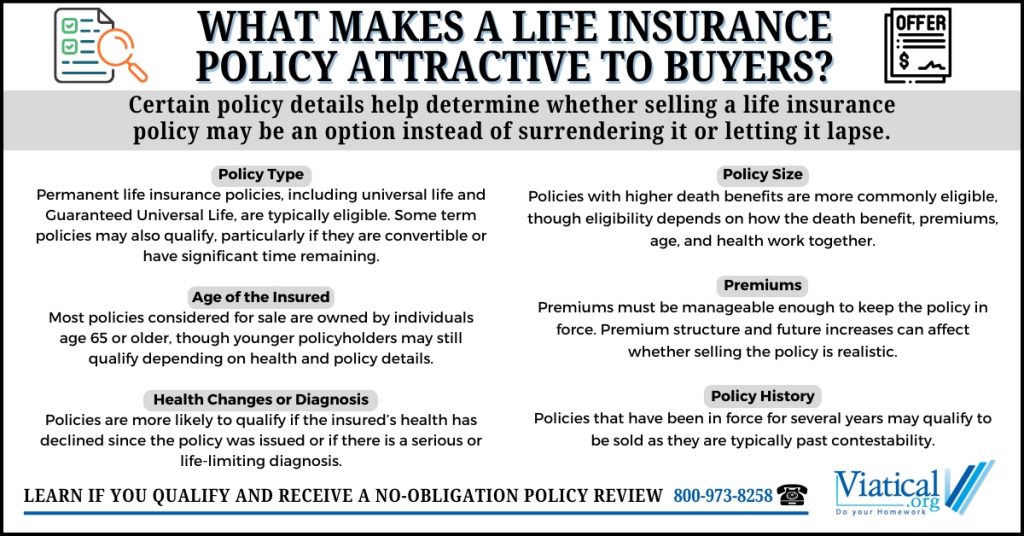

Policy Type Matters

The type of life insurance policy you have plays a major role in buyer interest.

Permanent policies such as universal life, Guaranteed Universal Life, whole life, and variable life are typically the most attractive because they are designed to remain in force for the insured’s lifetime as long as premiums are paid. Guaranteed Universal Life policies are often appealing because of their lower premium structure compared to traditional whole life policies, especially when coverage has been maintained as originally illustrated.

Term life insurance can also be attractive in certain situations. If the policy is convertible to a permanent policy or has a long remaining term, you may qualify to sell your term life insurance policy for cash. Short-term or non-convertible term policies are usually less appealing unless health factors significantly increase buyer interest.

Age of the Insured

Age is one of the first factors buyers consider. Policies owned by individuals over age 65 are generally more attractive, although younger policyholders may qualify if health has slipped.

As age increases, the potential timeframe for a buyer to receive the policy’s death benefit shortens, making the policy more economically viable from an investment perspective.

Health Status and Medical History

Health plays a critical role in determining whether a policy is attractive to buyers. Serious or chronic medical conditions often increase buyer interest because they can shorten life expectancy.

Buyers typically review medical records and may order a life expectancy evaluation. Conditions affecting the heart, lungs, kidneys, or nervous system are commonly evaluated, along with cancer diagnoses and progressive illnesses.

Changes in health that occurred after the policy was issued can significantly affect value.

Policy Size and Death Benefit Amount

The face value of the policy is another key factor. Buyers generally focus on policies with higher death benefits, often starting around $100,000, though this can vary based on age, health, and policy structure. Smaller policies may also qualify, depending on how these factors work together.

Premium Structure and Affordability

Buyers closely review premium requirements. Policies with stable, predictable premiums are generally easier to evaluate than those with rapidly increasing costs.

In some cases, a policy with higher premiums may still qualify, particularly when health factors are involved. However, policies with very high ongoing costs may be more difficult to maintain depending on the overall policy profile.

Policies with flexible premium structures or existing cash value can offer additional options for keeping coverage in force.

Length of Time the Policy Has Been in Force

Policies that have been in force for several years are often simpler to review than newer policies. Older policies have already passed key policy milestones, such as contestability periods, and tend to have more established premium and benefit structures.

Ownership and Beneficiary Structure

Clear ownership is important. Buyers want assurance that the policy owner has the legal right to sell the policy and that there are no unresolved ownership disputes.

Policies held in trusts, businesses, or shared ownership arrangements can still be sold, but they may require additional documentation and approvals. Clean ownership structures tend to move through the process more smoothly.

Why Buyer Interest Varies So Widely

No two policies are evaluated exactly the same way. A policy that is unattractive in one situation may be valuable in another based on health, age, and premium dynamics.

This is why many policyholders are surprised to learn that their life insurance policy may have much more value on the secondary market than through surrender or lapse.

Knowing When to Explore Your Options

If your policy is becoming expensive, unnecessary, or difficult to maintain, understanding what buyers look for can help you make a more informed decision.

To learn if you are likely to qualify for life settlements and learn more about your options, please give us a call at 800-973-8258