A life settlement for term insurance can provide an unexpected source of financial relief. While many people assume that term life insurance policies expire without any value, some can be sold for cash, even if they are nearing the end of their term. If you have a term policy you no longer need or can’t afford, a life settlement may be an option worth exploring.

What Is a Life Settlement?

A life settlement is the sale of an existing life insurance policy to a third party. In exchange for a lump-sum cash payment, the buyer takes over premium payments and becomes the new owner and beneficiary. Life settlements typically provide a higher payout than surrendering a policy or letting it lapse, and the funds can be used however you choose – whether for medical expenses, long-term care, or personal needs.

Can Term Life Insurance Be Sold?

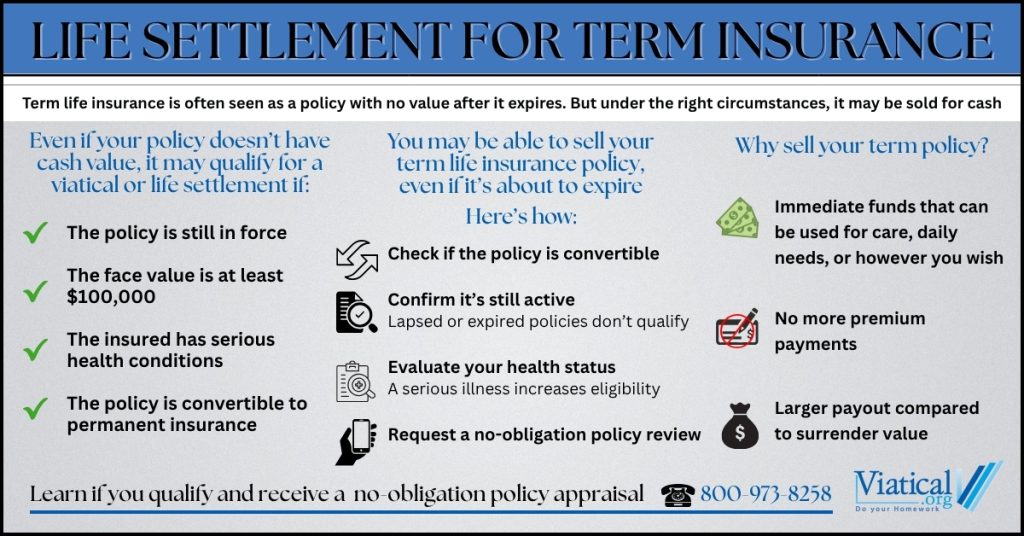

Yes, in some cases. Although term policies do not build cash value, certain types can qualify for a life settlement, including:

- Convertible term policies, which can be converted into permanent insurance

- Annual renewable term policies, if there is a buyer interested and the insured qualifies. Usually, if a policy is not convertible, the insured must have a life limiting condition.

Even if your term policy does not build value on its own, it may still be marketable if it meets the right criteria.

Who Qualifies for a Life Settlement for Term Insurance?

Eligibility typically depends on a combination of health, age, and policy details. In general:

- The insured is age 65 or older

- The policy has a face value of $100,000 or more

- The insured has a serious or chronic health condition for a viatical settlement although some may qualify for a life settlement even in better health

- The policy is still active and in good standing

If the policy is convertible, there is often more flexibility, even for older policies nearing expiration.

How Much Can You Get?

The amount you receive from a life settlement depends on several factors, including:

- The insured’s age and health condition

- The death benefit amount

- The cost of future premiums

- Whether the policy is convertible

- Market demand for policies like yours

Even though term policies don’t accumulate cash value, some can still sell for tens or even hundreds of thousands of dollars, especially if the policy is convertible and the insured meets buyer criteria.

Why Consider Selling a Term Life Policy?

A life settlement for term insurance can be an especially valuable option for individuals who:

- No longer need the coverage

- Can’t afford rising premiums

- Have outlived the policy’s original purpose (such as covering a mortgage or dependents)

- Want to fund medical care, retirement, or other pressing expenses

Rather than letting the policy lapse without any benefit, selling it gives you the chance to turn it into meaningful cash.

What Happens to the Policy?

After the sale:

- The buyer takes over premium payments

- They become the owner and beneficiary

- You receive a lump-sum payout

It is important to weigh your options and make sure this decision aligns with your financial goals and needs.

Many people assume that term life insurance holds no value once the term is over. But if you qualify, a life settlement for term insurance can unlock the hidden value in your policy. The cash you receive from a life settlement can be used to improve your quality of life or support your family’s financial needs.

To learn more or find out if your policy is eligible, contact Viatical or call 800-973-8258 for a no-obligation policy review.