A cancer diagnosis can bring not only emotional and physical challenges but also financial uncertainty. When it comes to life insurance and cancer diagnosis, many people don’t realize that an existing policy may offer living benefits through options like an accelerated death benefit or viatical settlement.

Accessing Your Policy While Still Living

Most people think of life insurance as something that only benefits loved ones after death. However, if you’ve been diagnosed with cancer, particularly advanced or terminal cancer, you may be able to access the value of your policy while you’re still alive.

Two primary options include:

1. Accelerated Death Benefit (ADB)

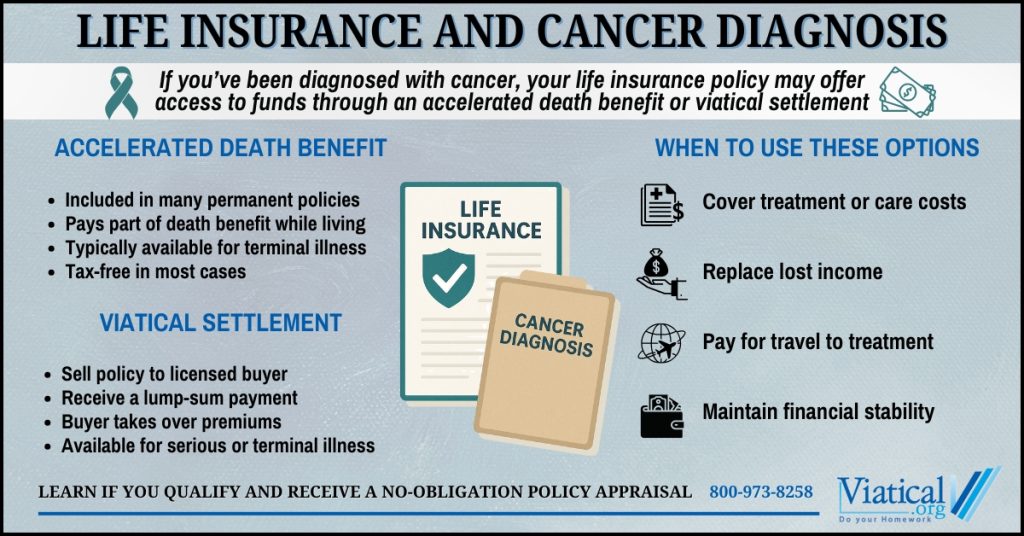

An accelerated death benefit is a rider included in many life insurance policies, especially permanent policies. It allows you to request a portion of your death benefit early if you have been diagnosed with a terminal illness, typically defined as a life expectancy of 12 to 24 months or less, depending on the insurer.

Key points about ADBs:

- You remain the policy owner

- The funds are usually tax-free

- The death benefit is reduced by the amount paid out

Not all policies include this rider automatically, and eligibility rules can vary. You’ll need to contact your insurance company to find out how to get an accelerated death benefit.

2. Viatical Settlement

A viatical settlement is another option that may allow you to access a larger amount of cash than an ADB, particularly if your policy does not include that rider or the payout is limited.

With a viatical settlement, you sell your life insurance policy to a licensed third-party buyer. In exchange, you receive a lump-sum cash payment. The buyer takes over premium payments and becomes the policy owner and beneficiary.

Viatical settlements are typically available if:

- You have a serious or terminal health condition. Life settlements may be available to those with a longer life expectancy.

- Your policy has a death benefit of at least $100,000

- The policy is whole life, universal life, or convertible term. Other types of policies may qualify – it is always best to ask.

Because buyers assess your life expectancy when making an offer, individuals with advanced-stage cancer may qualify for a higher payout.

Choosing the Right Option

Both options, accelerated death benefit and viatical settlement, can provide critical funds for:

- Treatment expenses

- In-home care or hospice

- Travel and housing for medical appointments

- Paying off debts

- Replacing lost income

- Travel or time with loved ones

The best choice depends on your specific policy, your diagnosis, and your financial needs. If your policy offers an ADB rider with a sufficient payout, it may be a good option. However, if you need a larger amount of cash or your policy doesn’t include that option, a viatical settlement may be worth exploring. Sometimes, you may be able to sell the remaining portion of your policy in a viatical settlement after taking an accelerated death benefit.

A cancer diagnosis doesn’t mean you’re limited to waiting for your policy’s death benefit to be paid to your beneficiaries. If you own a life insurance policy, take the time to explore whether you qualify for an accelerated death benefit or viatical settlement. These options can offer real financial relief when it’s needed most.

If you’d like to learn if your policy qualifies for a viatical settlement, contact us for a no-obligation policy review and appraisal. 800-973-8258