Many policyholders want to know, can I sell my life insurance policy without a medical exam? The answer is yes. When you sell a policy through a life settlement or viatical settlement, potential buyers review your existing medical records instead of requiring a new exam. These records provide enough information for buyers to evaluate your health history and determine your policy’s potential value, without any additional testing or appointments.

How Medical Records Are Used Instead of Exams

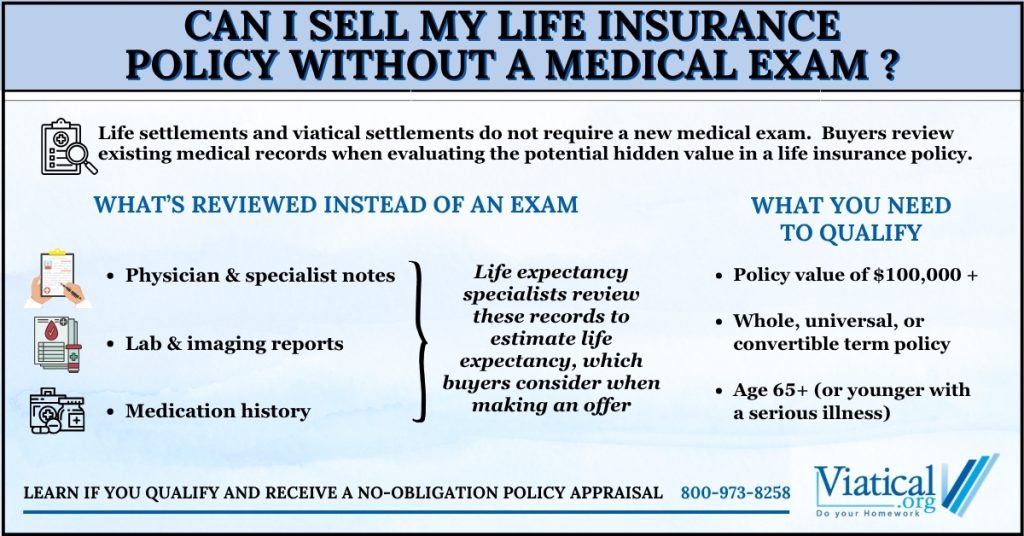

When you sell a life insurance policy, the buyer needs to assess the risk and potential payout. To do this, life settlement purchasers review your current medical records instead of scheduling an exam. This typically includes:

- Recent physician or specialist reports

- Hospital discharge and treatment summaries

- Lab tests and imaging results

- Prescription and medication histories

Life expectancy specialists review these records to provide an estimate of life expectancy, which buyers consider when determining a policy’s potential settlement value.

Why a New Exam Is Not Necessary

Unlike applying for new coverage, selling an existing policy does not require underwriting for approval. Buyers are only interested in understanding how long the policy might remain in force and the expected costs of maintaining it. Your current medical documentation is sufficient to make this determination and allows for a viatical settlement without medical exam.

By using existing records, the process is streamlined. Settlement companies can access the necessary information directly from your healthcare providers with your consent, without the need for additional medical visits.

Factors That Determine Eligibility

Although a medical exam is not needed, there are still general requirements for selling a life insurance policy:

- Policy Type: Universal life, whole life, or convertible term policies are commonly accepted.

- Death Benefit Amount: Policies with a face value of $100,000 or more are typically preferred.

- Age or Health Condition: Older age (65+) or a serious illness may result in higher settlement offers.

These factors are assessed using your insurance details and medical history.

How to Begin the Process

- Request a Quote: Provide your policy details such as coverage amount, premiums, and type.

- Authorize Record Access: The life settlement company obtains copies of your medical and insurance records.

- Review Offers: Once the evaluation is complete, you will receive offers based on the policy’s market value if there are interested direct buyers.

So, can I sell my life insurance policy without a medical exam? Yes, if you qualify. Life settlement buyers rely on your existing medical records to assess your policy’s value, allowing you to move forward without unnecessary testing. Your existing health records are all that’s needed to determine what your policy may be worth.

To learn if you qualify for a viatical settlement or life settlements, please give us a call at 800-973-8258. It usually only takes a 5–10 minute call to learn if your existing life insurance policy may have a hidden value.

Frequently Asked Questions

1. Do I need to collect my medical records myself?

No. With your signed authorization, the settlement company will request the necessary medical records directly from your healthcare providers.

2. How long does it take to receive an offer?

Most policy reviews take only 1-2 weeks once medical and insurance records are obtained.

3. Does the review process affect my policy or coverage?

No. Requesting a quote or evaluation does not impact your coverage. You remain the policy owner until you accept an offer and complete the sale.