Most people believe their only options with a life insurance policy are simple: keep it or cancel it.

That assumption is costing policyholders billions of dollars every year.

What many don’t realize is that a life insurance policy is a financial asset that can often be sold for significantly more than its cash surrender value through a life settlement.

If you’re wondering “Should I sell my life insurance policy?”, the answer depends on your situation. Below are the top 10 reasons people choose to sell their life insurance policy.

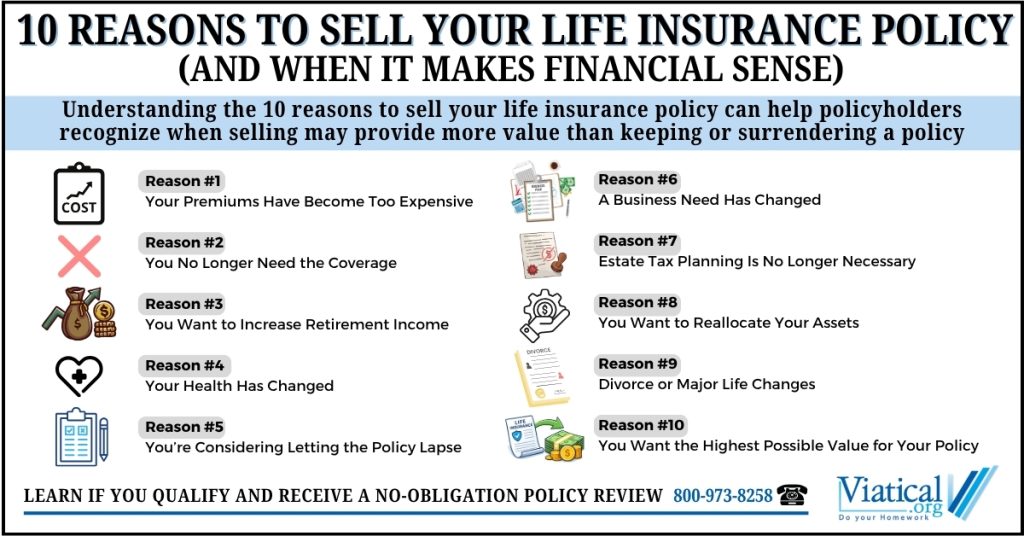

Reason #1 Your Premiums Have Become Too Expensive

What happens if I can’t afford my life insurance premiums?

As policies age, especially universal life and whole life insurance, premium costs often increase dramatically.

Many retirees face a difficult choice:

• Continue paying thousands per year

• Let the policy lapse and lose everything

A life settlement provides a third option:

• Sell your life insurance policy for cash instead of losing it

In many cases, policyholders receive 3 to 10 times more than the surrender value.

Reason #2 You No Longer Need the Coverage

Can I sell my life insurance if I don’t need it anymore?

Life insurance is typically purchased for a specific reason:

• Income replacement

• Mortgage protection

• Family security

But over time:

• Children become financially independent

• Debt is paid off

• Retirement assets grow

When the original need disappears, the policy becomes an unnecessary expense and a hidden asset.

Reason #3 You Want to Increase Retirement Income

Can I use my life insurance for retirement income?

Yes. This is one of the fastest growing reasons people sell.

Instead of:

• Drawing down investments

• Increasing portfolio risk

A life settlement can provide:

• Immediate lump sum cash

• Supplemental retirement income

• Funds for lifestyle or healthcare

Reason #4 Your Health Has Changed

Does poor health increase life settlement value?

Yes. This is one of the most misunderstood aspects of life settlements.

When health declines:

• Life expectancy shortens

• Policy value in the secondary market increases

That means:

• The worse your health, within reason, the higher the potential offer

This is why viatical settlements exist and why timing matters.

Reason #5 You’re Considering Letting the Policy Lapse

Is it better to sell or surrender a life insurance policy?

Let’s break this down clearly:

• Lapse: $0

• Surrender: Minimal cash value

• Sell through a life settlement: Often the highest payout

If you are already thinking about canceling your policy, a life settlement should always be evaluated first.

Reason #6 A Business Need Has Changed

What happens to key man or buy sell insurance if a business changes?

Many policies are purchased for business purposes:

• Key person insurance

• Buy sell agreements

• Executive compensation plans

But when:

• A business is sold

• A partner exits

• The company restructures

The policy may no longer be needed.

Instead of canceling, business owners can:

• Convert the policy into liquidity

• Redeploy capital into the business or other investments

Reason #7 Estate Tax Planning Is No Longer Necessary

Do I still need life insurance for estate taxes?

Recent increases in estate tax exemptions have reduced the need for many policies originally purchased for estate planning.

As a result:

• Policies inside trusts, often called ILITs, may no longer serve their original purpose

• Families are left paying premiums for outdated strategies

Selling the policy can:

• Unlock capital

• Improve overall estate efficiency

Reason #8 You Want to Reallocate Your Assets

Is life insurance the best use of my money right now?

For many policyholders, the answer becomes no over time.

Selling a policy allows you to:

• Pay off debt

• Fund long term care

• Invest in higher return opportunities

• Improve liquidity

Reason #9 Divorce or Major Life Changes

Can I sell a life insurance policy after divorce?

Yes. It is common.

After divorce or major life transitions:

• Beneficiaries may no longer be relevant

• Financial priorities change

Rather than maintaining a policy tied to the past, many individuals choose to:

• Liquidate the asset

• Reallocate funds toward their new financial plan

Reason #10 You Want the Highest Possible Value for Your Policy

What is my life insurance policy actually worth?

This is the most important question and the one most people never ask.

Insurance companies only show you:

• The surrender value

But the true market value may be significantly higher.

That’s because:

• Institutional buyers compete to purchase policies

• The secondary market determines value, not the carrier

This creates an opportunity to:

• Unlock hidden value most policyholders never realize exists

The Key Insight: Your Policy Is an Asset Not Just Insurance

Most policyholders lapse or surrender their policy without ever knowing they could sell it.

This happens because:

• Insurance companies are not required to disclose life settlements

• Traditional advisors often do not specialize in this market

As a result, billions in policy value are lost every year.

Who Typically Qualifies for a Life Settlement?

Am I eligible to sell my life insurance policy?

While every case is different, most qualified sellers meet the following criteria:

• Age 65 or older, or serious health condition

• Policy size $100,000 or more, ideally $250,000 or more

• Type of policy such as universal life, whole life, or convertible term

• Premiums that are no longer desirable

Life Settlement vs Surrender: Why This Decision Matters

What’s the difference between surrendering and selling?

Surrendering returns the policy to the insurance company and typically provides only the cash surrender value.

Selling transfers the policy to a third-party buyer through a life settlement and may produce a significantly higher payout.

What Should You Do Next?

If any of the situations above apply to you, the next step is simple:

Find out what your policy is actually worth.

• It only takes about 5 to 10 minutes

• No cost to evaluate

• No obligation

And it could reveal:

• Tens or even hundreds of thousands of dollars in hidden value

Should you sell your life insurance policy?

You should consider selling your life insurance policy if you no longer need the coverage, cannot afford the premiums, or want to access the policy’s value while you are still alive. A life settlement often provides more value than surrendering or lapsing the policy, especially for individuals over age 65 or those with health changes. To learn more about your options for accessing your policy’s hidden value, please give us a call at 800-973-8258