If you have chronic kidney disease and are considering selling a life insurance policy with chronic kidney disease, you’re not alone. Many individuals facing serious health conditions explore life settlements as a way to unlock the value of their policies to cover medical expenses, caregiving costs, or other financial needs.

What Is Chronic Kidney Disease?

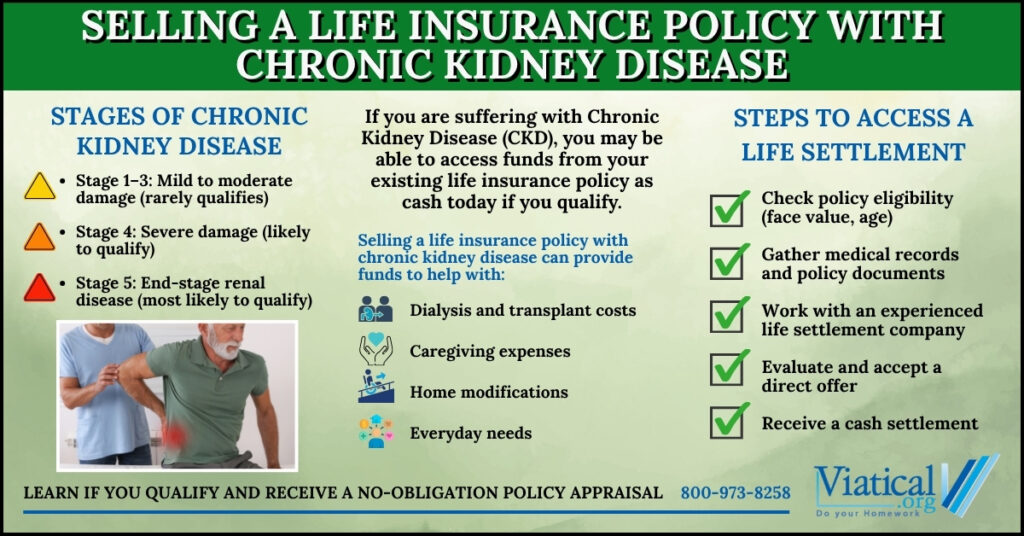

Chronic Kidney Disease (CKD) is a progressive condition where the kidneys gradually lose function over time. It’s typically divided into five stages, with Stage 5, also called end-stage renal disease (ESRD), being the most severe. At this stage, the kidneys can no longer filter waste effectively, and patients often require dialysis or a kidney transplant.

When Can You Qualify for a Life Settlement?

While any stage of CKD can potentially qualify, life settlement companies generally look for:

- Stage 4 CKD: Severe kidney damage with an estimated glomerular filtration rate (eGFR) of 15–29 mL/min. Symptoms may include fatigue, swelling, and high blood pressure.

- Stage 5 (ESRD): Complete or near-complete kidney failure (eGFR <15 mL/min). Dialysis or transplant is typically required. This stage is most likely to qualify for a viatical settlement, especially if dialysis has begun.

The earlier stages (1–3) are usually less likely to qualify for life settlements unless combined with other serious conditions or complications.

Common Treatments and Therapies

Understanding the therapies commonly used for CKD is essential, as life settlement providers often review medical records:

- Medications:

- ACE inhibitors (e.g., lisinopril) and ARBs (e.g., losartan) to control blood pressure and protect kidney function.

- Diuretics (e.g., furosemide) to reduce swelling.

- Phosphate binders (e.g., sevelamer) to control phosphorus levels.

- Erythropoiesis-stimulating agents (e.g., epoetin alfa) to treat anemia.

- Calcimimetics (e.g., cinacalcet) for managing secondary hyperparathyroidism.

- Dialysis: For ESRD patients, either hemodialysis (in-clinic) or peritoneal dialysis (at home) is used to remove waste from the body.

- Kidney Transplant: Considered for suitable candidates in ESRD.

Why Consider Selling Your Life Insurance Policy?

- To cover costly dialysis treatments and medications.

- To pay for in-home care or transportation to dialysis centers.

- To relieve financial pressure on loved ones.

- To fund home modifications that may be needed due to CKD-related complications.

What Should You Know?

Not all life insurance policies can be sold. Policies with a face value of at least $100,000 and owned for a minimum period (often two years) are more likely to qualify. Generally, qualifying insureds are 65 or older, but in advanced stages of the disease, some younger patients may qualify. You’ll need to provide access to comprehensive medical records, including your CKD stage and treatments.

If you’re navigating the challenges of chronic kidney disease and need financial support, selling a life insurance policy with chronic kidney disease could provide a valuable solution. By working with an experienced life settlement company, you can unlock the hidden value in your life insurance policy to help cover medical expenses, caregiving needs, or simply provide peace of mind during a difficult time. Explore your options today and discover how your life insurance policy can work for you when you need it most.

It usually only takes a 5-10 minute phone call to learn if you qualify. 800-973-8258