A diagnosis of leukemia often brings immediate financial concerns alongside medical decisions. Selling your life insurance policy when you have leukemia may provide access to funds that can help cover treatment costs, replace lost income, or improve quality of life during a difficult time. Many policyholders do not realize that a life insurance policy may be treated as a financial asset that can be sold for cash while they are still alive.

Can Leukemia Patients Qualify for a Viatical Settlement?

Individuals diagnosed with leukemia frequently qualify for a viatical settlement depending on disease progression, treatment status, and overall medical outlook. Viatical settlements are designed for people facing serious or life-threatening illnesses who need access to liquidity while managing medical care and related expenses.

Eligibility is typically based on several factors:

- Type of leukemia and stage of disease

- Treatment history and physician prognosis

- Life expectancy evaluations

- Policy size and structure

- Ability or desire to continue paying premiums

Both acute and chronic forms of leukemia may qualify. Patients actively receiving chemotherapy, targeted therapy, immunotherapy, or preparing for stem cell transplantation may still be eligible depending on medical circumstances.

Why Selling a Policy May Be Considered

Leukemia treatment often involves ongoing care, hospital visits, medication costs, and extended recovery periods. Even individuals with strong health insurance coverage may face significant out-of-pocket expenses or reduced income during treatment.

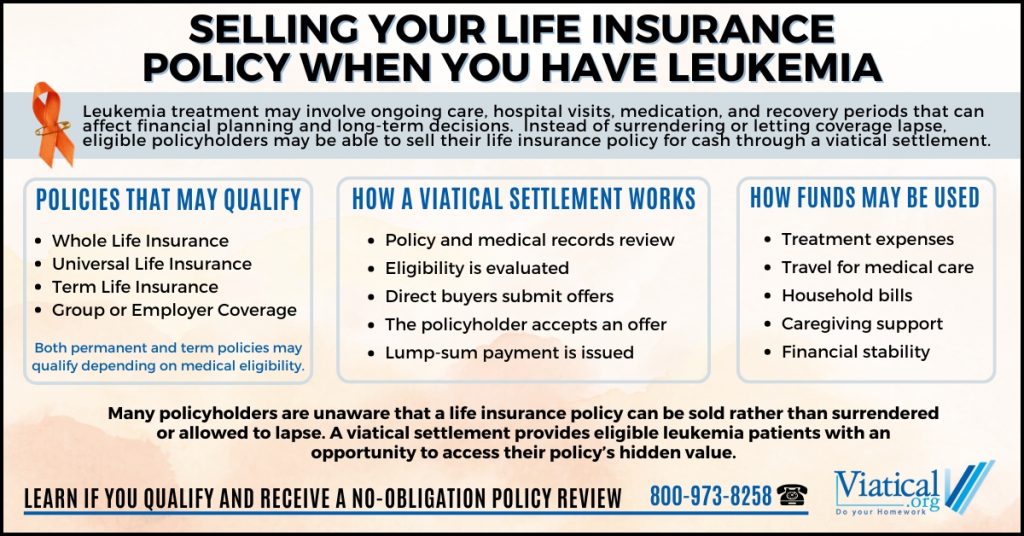

A viatical settlement may provide funds that can be used for:

- Specialized or advanced treatment options

- Travel related to medical care or second opinions

- Household expenses during time away from work

- In-home assistance or caregiving support

- Paying down debt or improving financial stability

Rather than surrendering a policy for minimal value or allowing coverage to lapse due to rising premiums, selling the policy may allow the policyholder to receive a lump-sum payment that is often substantially higher than the surrender value.

Types of Life Insurance Policies That May Qualify

Many policyholders assume that only life insurance policies with cash value can be sold, or that term coverage has little or no market value. In reality, leukemia patients may qualify with several types of life insurance coverage, including both permanent and term policies.

Policies that may qualify include:

- Whole life insurance

- Universal or adjustable life insurance

- Term life insurance policies

- Convertible term policies

- Certain employer or group life insurance policies

Permanent policies are commonly eligible because they remain in force for life, but term policies may also qualify when the insured’s medical condition meets buyer criteria and coverage is still active. Even policies without accumulated cash value can sometimes be sold rather than surrendered or allowed to lapse.

How the Viatical Settlement Process Works

The process of selling a life insurance policy generally follows several steps:

- Policy information and medical records are reviewed.

- Life expectancy assessments are completed.

- Licensed institutional buyers evaluate the policy.

- Offers are presented to the policyholder.

- Upon acceptance, ownership transfers and payment is issued.

After the sale is completed, the buyer assumes responsibility for future premium payments and ultimately receives the death benefit. The policyholder receives immediate cash proceeds and no longer has ongoing obligations tied to the policy.

An Alternative to Letting Coverage Lapse

Each year, billions of dollars in life insurance coverage lapse simply because policyholders are unaware that a secondary market exists. When circumstances change after a leukemia diagnosis, some policyholders begin reevaluating whether keeping their life insurance policy still aligns with their current financial priorities. After a leukemia diagnosis, some policyholders choose to explore options other than maintaining coverage that may no longer serve its original purpose.

Selling a life insurance policy can convert an underused or unaffordable asset into valuable financial support. For individuals living with leukemia, accessing the value of an existing policy may provide flexibility, financial relief, and greater control over financial decisions during treatment and recovery.

To learn if you qualify and for a no-obligation policy appraisal, please give us a call today at 800-973-8258.