Many former service members are unaware that they may be able to turn an existing life insurance policy into immediate cash. This veteran’s guide to life settlements and viatical settlements explains how these options work, who qualifies, and how veterans can benefit especially those holding convertible term life insurance policies that are nearing expiration.

What Are Life Settlements and Viatical Settlements?

Life settlements allow a policyholder to sell a life insurance policy they no longer need in exchange for a lump-sum cash payment that exceeds the surrender value.

A viatical settlement is similar but applies when the insured has a serious or terminal illness, often providing even higher payouts because of shorter life expectancy.

Both types of settlements give policyholders a way to access hidden value that might otherwise be lost if a policy lapses or is surrendered for a minimal amount. This can make a major difference for veterans who may be managing health challenges, fixed incomes, or unexpected expenses after leaving service.

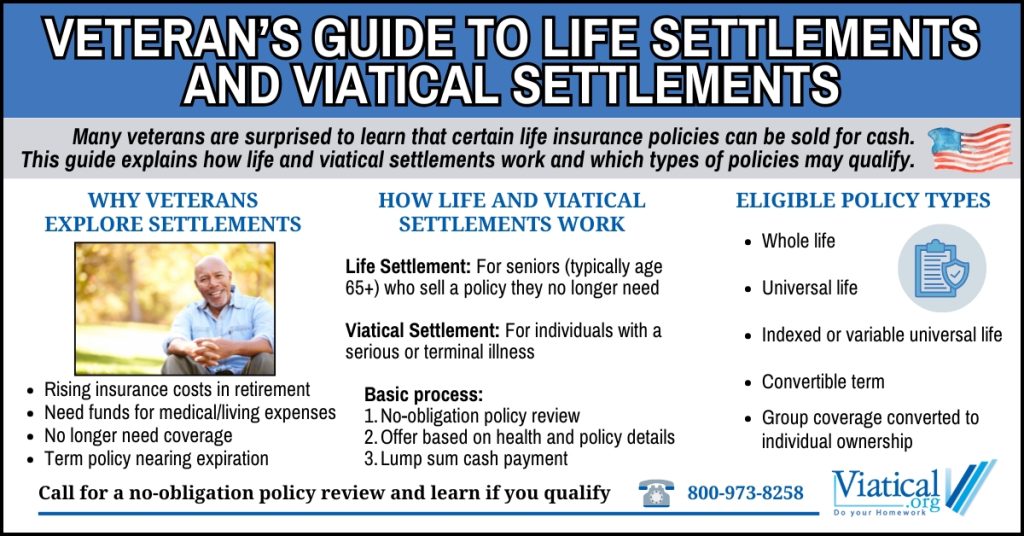

Why Veterans Consider Selling a Policy

After active duty or federal employment, veterans often carry private life insurance policies purchased outside of government programs. These policies were meant to protect loved ones, but over time, premiums can become difficult to maintain. Others find that they no longer need the same level of coverage once their children are grown or financial responsibilities have changed.

Selling a qualifying life insurance policy can provide much-needed cash for:

- Out-of-pocket medical or prescription costs

- Long-term care or assisted living expenses

- Mortgage payments or home modifications

- Everyday living and retirement needs

Instead of letting a policy lapse, a life or viatical settlement can transform it into immediate, usable funds.

Convertible Term Policies: A Hidden Opportunity

Many veterans have term life insurance from a private insurer or former employer. If the policy is convertible, it may be eligible for a life or viatical settlement. Eligibility depends on the presence of that conversion option. Non-convertible term policies can occasionally qualify, but only in rare cases. Most buyers prefer policies that include the option to convert to permanent coverage.

If you have a convertible term policy nearing the end of the original term, premiums will likely increase exponentially if the policy is retained as an annual renewable term policy. This is why, in many cases, people choose to lapse expiring term insurance. A life settlement for term insurance can provide an alternative by allowing you to access hidden value that would otherwise be lost.

Eligibility for Veterans

Each policy is evaluated individually, but veterans may qualify if they:

- Are age 65 or older or have a serious or terminal health condition

- Own a qualifying life insurance policy with a death benefit of at least $100,000

Policies that may qualify include:

- Whole life insurance

- Universal life insurance

- Indexed universal life or variable universal life

- Convertible term life policies

- Survivorship or joint life insurance

- Group life policies that have been converted into individual ownership

- FEGLI policies that have been converted to a private plan through an approved carrier

Because qualification is determined by specific policy terms and individual circumstances, veterans should have their coverage evaluated to understand what options may be available.

How to Get Started

A no-obligation policy review is the first step in understanding whether your life insurance policy could qualify for a life or viatical settlement. This review provides clarity about your policy’s potential value and helps you make an informed decision.

A policy review can show veterans what choices exist before a policy lapses or expires. To learn more, please give us a call at 800-973-8258. It only takes a short 5-10 minute phone call to learn if you are likely to qualify.