People are often surprised to learn that the cash value shown by their insurance company doesn’t reflect what their policy may actually be worth. What is the cash value of a life insurance policy? It’s the amount your insurer lists as available if you surrender or borrow against your policy. But that figure represents only what the insurance company is willing to pay, not its potential market value. In many cases, a life insurance policy can be worth significantly more when sold through a life settlement or viatical settlement in the secondary market.

How Insurers Define Cash Value

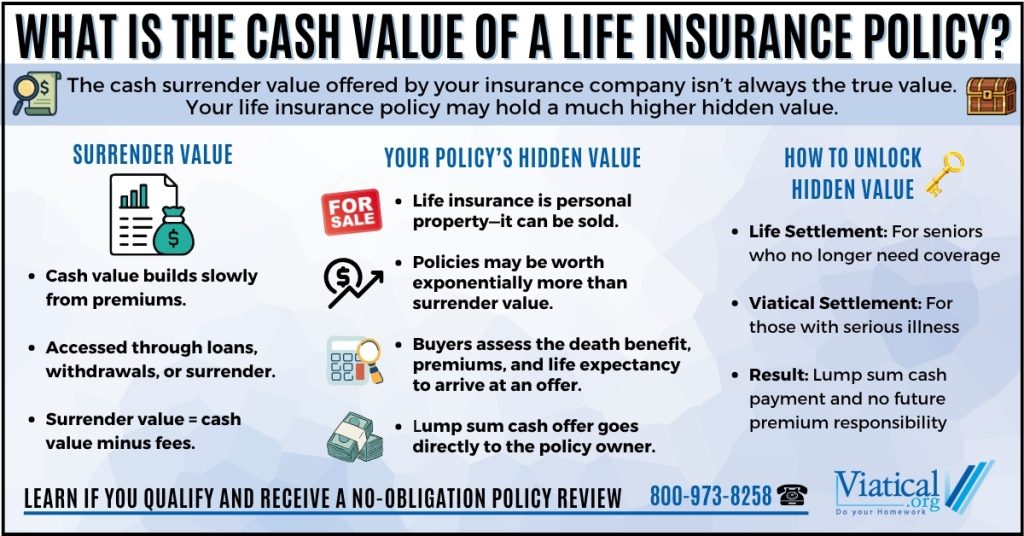

Cash value is an internal account within a whole life, universal life, or variable life insurance policy. It builds gradually as you pay premiums and earns interest or investment returns. Over time, this balance can grow into a sum that the insurer allows you to access through loans, withdrawals, or by surrendering the policy.

However, when you surrender a policy, you only receive the cash surrender value, which is the cash value minus any fees, loans, or penalties. That payout is typically a fraction of the total premiums you’ve paid over the years and far less than what your policy could be worth to an investor.

Hidden Value in Life Insurance

Your life insurance policy is a financial asset that often has a hidden value that most policyholders never realize is there. In the secondary market for life insurance, qualified buyers may be willing to pay much more than the surrender value offered by the insurance company because they evaluate the policy differently.

Investors look at the face amount (death benefit), premium schedule, and your estimated life expectancy to calculate what they’re willing to offer. As a result, many people receive lump-sum payments that are on average 6.5 times more than their policy’s cash surrender value. This is especially true for seniors or individuals with serious health conditions.

Life Settlements vs. Viatical Settlements

- Life settlements typically involve a senior (someone 65 or older) who sells their life insurance policy for more than the surrender value but less than the death benefit.

- A viatical settlement applies when the insured has a serious or terminal illness and needs immediate financial support for care, medical expenses, or quality of life.

In both cases, ownership of the policy transfers to a direct buyer who takes over premium payments and becomes the policy owner and beneficiary. The policyholder receives an immediate cash payment and is not longer responsible for premium payments.

Why the Market Value Can Be Much Higher

Insurance companies calculate cash value using conservative formulas designed to limit their liability. The secondary market for life insurance, which includes regulated life settlement and viatical settlement companies, operates differently. These buyers compete to purchase qualifying policies, often offering substantially more than the insurer’s stated value.

That’s why understanding your policy’s true market value is essential before surrendering or letting it lapse. Many policyholders who thought their coverage had little value discover that it’s worth exponentially more when appraised as a life settlement for viatical settlement. Even term policies or those with no cash value can often qualify.

Finding Out What Your Policy Is Really Worth

If you’re reviewing your life insurance options, don’t rely solely on the insurer’s stated cash value. You may have an asset that can be sold for far more in today’s market. Getting a no-obligation appraisal can help reveal your policy’s potential hidden value and give you a clearer picture of your available options.

To learn if you qualify, please give us a call today at 800-973-8258.