Viatical Life Settlement Case Studies

Examples Viatical Life Settlement Case Studies

Learn from some past viatical and life settlement examples. We have put together a list of viatical life settlement case studies so you will get an idea of some cash payments and how viatical settlements and life settlements are used. Learn how much your policy is worth as a life settlement or viatical settlement by filling out our contact form. Please call us at 800-973-8258 if you have immediate needs or would like to speak to someone in person.

- 2026 Viatical Settlement Examples

These 2026 viatical settlement examples show how real policyholders have turned life insurance policies into immediate cash, often receiving far more than the surrender value or letting a policy lapse. Each case highlights how age, health, policy type, and face value can impact the amount a policy may be worth in the secondary market. How These Examples Should Be Viewed Every life settlement or viatical settlement is evaluated individually. Buyers review medical records, policy details, and premium obligations together to determine value. These examples are meant to provide realistic expectations, not guarantees. The only way to determine what a policy …See More

These 2026 viatical settlement examples show how real policyholders have turned life insurance policies into immediate cash, often receiving far more than the surrender value or letting a policy lapse. Each case highlights how age, health, policy type, and face value can impact the amount a policy may be worth in the secondary market. How These Examples Should Be Viewed Every life settlement or viatical settlement is evaluated individually. Buyers review medical records, policy details, and premium obligations together to determine value. These examples are meant to provide realistic expectations, not guarantees. The only way to determine what a policy …See More - Long Term Assisted Living Payment AssistanceThe mother of this family was simply unable to continue living at home and the family was considering all of their Nursing Home options. They realized early on that they would likely need help with paying for assisted living. At the same time, the family was also preparing to surrender their mother’s $100,000 Universal Life Insurance policy as they were getting ready to apply to a Medicaid approved Nursing Home. The family was helpful and very quick in gathering their mother’s policy information and medical records. Their mother was quickly able to move into their first choice of Nursing Homes. The …See More

- Convert Life Insurance Into a Long Term Care Benefit PlanConvert Life Insurance into a Long Term Care Benefit Plan, even if it has no cash value or a large loan. Recently, a daughter was exploring funding options, as her father was in need of long term care in an assisted living community. The family was paying for their father’s care and their funds were dwindling, but they did not want to be forced to move their father into a particular nursing home. The father owned a few life insurance policies and wished to convert one $50,000 life insurance policy which had an $18,000 loan. His life insurance policy did …See More

- Sell Your Life Insurance Policy for Cash to Pay for Assisted LivingIf you do not need or cannot afford your life insurance policy, you can now sell your life insurance policy for cash to pay for assisted living. It is not uncommon for an elderly couple to both require elder care at the same time. Recently, a married couple converted their life insurance policies into Medicaid life settlement plans to pay for assisted living. The wife was her husband’s primary care provider and unfortunately suffered a stroke of her own. Because she was no longer able to provide home care to her husband and was also no longer able to care …See More

- Dual Assisted Living Conversion Case Study, Emeritus of Lake PointThe business office director at Emeritus of Lake Point, GA contacted us with a family requiring financial assistance for a wife and husband. The wife owned $376,000 of life insurance that they wanted to know if they could trade in for a Viatical Assisted Living Conversion. They were planning to abandon the policies and not sure how they would pay for their care or a nursing home if necessary. Once they were informed that they had the legal right to convert their life insurance to cover costs of long term care, they moved quickly to submit an application. After completing the enrollment …See More

- Case Study: Budget Shortfall in Long Term CareThe Business Office Director of the Heartfields at Cary in North Carolina contacted us about a married couple in residence needing funding help to address a budget shortfall and their growing debt to the community. They both own long term care insurance policies but did not yet qualify to trigger all of their benefits. They also had applied for the VA benefit and were notified that they qualify but were not sure when the benefit will start. Still facing a financial gap in their ability to keep pace with their monthly commitment to the Heartfields of Cary; the family decided …See More

- Case Study: Medicaid Spend Down Path, Convert Life Insurance and Remain at ResidenceA father was already a resident at Eldorado Heights in Klamath Falls, OR and already on a Medicaid spend down path. The family inquired about a Viatical Assisted Living Conversion as they were attempting to convert an existing life insurance policy and still extend his ability to remain in residence. He owned a $100,000 life insurance policy that they were advised to not keep because they were spending down for eventual Medicaid eligibility and the policy would count against them as an asset. The policy had $5,000 of cash value and a $2,000 loan. Within thirty days of submitting an …See More

- Case Study: Viatical Assisted Living Conversion Affecting Quality of LifeBrookdale Senior Living introducing the Viatical Assisted Living Conversion concept to Brookdale’s communities across the United States in February. After only the first month, Viatical.org is pleased to share this successful case study. This most recent Viatical Assisted Living Conversion truly affected the quality of life for the underlying family. A Viatical Assisted Living Conversion converts an in-force life insurance policy into an immediate payout long term care benefit. Qualifying for the conversion is usually quick, uncomplicated, and can often be completed in as little time as 30 days. Brookdale Place at San Marcos The applicant and his wife wanted …See More

- Secure Assisted Living Payments for Stroke CareThe family was given our information from the Whitcomb of St. Josephs, MI. It became necessary to move both parents into an assisted living facility as their mother recently had a stroke and was no longer able to care for herself or her husband. Upon learning that they could convert a group policy their father had kept after retirement; they completed an application for both parents…

- Alzheimer’s Assisted Living Funding Case StudyA wife was caring for her husband, an Alzheimer’s victim, at home and needed to move him into a memory care facility for safety reasons. She was researching communities in the Atlanta, GA area and was also looking for funding options to help pay for the costs of housing and care. She found out about the Viatical Assisted Living Conversion online and learned that they could convert their $250,000 life insurance policy into a long term care payout…

Call for an appraisal before you attempt to sell your life insurance policy for cash.

Learn More About Viaticals and Life Settlements

- Can You Sell a Policy with an Irrevocable Beneficiary?

- Can a Life Insurance Policy in an Irrevocable Trust Be Sold?

- Life Settlement Brokers Create Regulatory Risks for RIAs

- 2025 Life Settlement Market Data

- Life Insurance Quotes and Policy Exit Strategies for Estate Planners, Tax Attorneys, and CPAs

- 2026 Viatical Settlement Examples

- Direct to Consumer Viatical Settlements

- How Sick Do I Have to Be for a Viatical Settlement?

- Can You Sell a Life Insurance Policy That Is About to Lapse?

- Can You Sell a Joint Life Insurance Policy for Cash?

- What Types of Life Insurance Policies Can Be Sold for Cash?

- Top 20 Questions Policyowners Ask Before Selling a Life Insurance Policy

- Selling Your Life Insurance Policy When You Have Leukemia

- How Much Do Life Settlement Companies Pay

- What Documents Are Needed for a Viatical Settlement?

- Can You Sell a Term Life Insurance Policy Without Converting It First?

- What Happens If You Stop Paying Life Insurance Premiums?

- Viatical Settlements and Living Longer Than Expected

- Do Beneficiaries Have to Agree to a Viatical Settlement?

- What Makes a Life Insurance Policy Attractive to Buyers?

- Life Insurance Options After a Life-Changing Diagnosis

- Do Viatical Settlements Affect Medicare?

- Can a Viatical Settlement Help with Rehabilitation Costs?

- Check Your Term Policy’s Conversion Options Before It Expires

- Can a Life Settlement Help Pay for Skilled Nursing Care?

- Veteran’s Guide to Life Settlements and Viatical Settlements

- Using Life Insurance to Pay for Home Modifications

- A Life Settlement Could Help Pay for an Elderly Parent’s Care

- Viatical Settlements for Patients with Pulmonary Hypertension

- A Second Opinion Could Boost Your Viatical Settlement Payout

- Do Life Settlements Affect Social Security?

- Can You Sell Part of Your Life Insurance Policy?

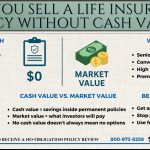

- What Is the Cash Value of a Life Insurance Policy?

- Can You Pay Medical Bills with Life Insurance?

- Using Life Insurance to Pay for Long-Term Care

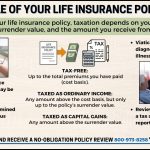

- How the Sale of Your Life Insurance Policy Is Taxed

- Get a Viatical Settlement in Your State

- Can a Young Person with Cancer Sell Their Life Insurance?

- Selling Your Insurance Policy When You Have Cancer

- How to Find Life Insurance Policy Buyers

- Paying for In Home Care Services with Term Life Insurance

- Can You Sell Your Life Insurance Policy After a Stroke?

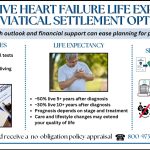

- Congestive Heart Failure Life Expectancy and Viatical Settlement Options

- Chemotherapy Costs and How a Viatical Settlement Can Help

- Viatical Settlements for Ovarian Cancer

- Cystic Fibrosis and Viatical Settlements

- Viatical Settlements for Multiple Sclerosis

- Can You Sell a Life Insurance Policy Without Cash Value?

- Is Selling Your Life Insurance Policy an Option?

- How to Get the Best Viatical Settlement

- Financing Chronic Illness

- Financial Options for Bile Duct Cancer Patients with Life Insurance

- Viatical Options for Head and Neck Cancer

- Access Life Insurance Funds After a Mesothelioma Diagnosis

- Life Settlement for Term Insurance

- Life Insurance and Cancer Diagnosis

- Can I Sell My Life Insurance Policy Without a Medical Exam?

- Viatical Settlements for Autoimmune Disease Patients

- Cash from Life Insurance with Advanced Dementia

- How to Get a Life Insurance Policy Valuation If You’re Terminal

- Selling Life Insurance with Stage 4 Colon or Rectal Cancer

- Access Life Insurance Funds After a Myeloma Diagnosis

- Victims of Metastatic Bone Cancer Can Get Cash from Life Insurance

- Viatical Settlements for Patients with Lung Cancer

- Viatical Settlements for Patients with Liver Disease

- Viatical Settlements for Patients with Diabetes

- How to Pay for Elder Care Without Long-Term Care Insurance

- Viatical Settlements for Patients with Pulmonary Fibrosis

- Selling Life Insurance with Advanced COPD

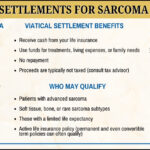

- Viatical Settlements for Sarcoma Patients

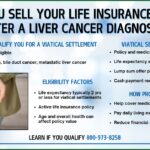

- Can You Sell Your Life Insurance Policy After a Liver Cancer Diagnosis?

- How a Viatical Settlement Can Help When Cancer Comes Back

- Getting Cash from Life Insurance with Metastatic Melanoma

- Selling a Life Insurance Policy with Chronic Kidney Disease

- Why Cancer Patients Are Turning to Viatical Settlements

- Viatical Settlements for End of Life Care

- Viatical Settlements for Patients with Pancreatic Cancer

- Huntingtons Disease and Viatical Settlement Eligibility

- Who Qualifies for a Viatical Settlement in 2025?

- Qualifying for a Viatical Settlement with Severe Amyloidosis

- Glioblastoma Life Insurance Payout

- Get Enhanced Cash Value from Your Universal Life Insurance

- Viatical Settlements for Patients with Stomach Cancer

- Viatical Settlements for Patients with Heart Disease

- Does Stage 4 Cancer Always Qualify for a Viatical Settlement?

- Define Life Expectancy and Why It Matters in a Viatical Settlement

- Ways to Get the Most Cash for Your Life Insurance

- Is Selling Your Life Insurance Worth It?

- How to Get an Accelerated Death Benefit

- How to Get a Viatical Settlement Quote Online

- Stop Paying for Life Insurance You Don’t Need

- Viatical Settlement Companies Near Me

- Why Your Insurance Company Might Not Tell You About Life Settlements

- How Fast Can I Get Money from a Viatical Settlement?

- Selling Your Life Insurance Policy

- Selling a Premium Financed Life Insurance Policy for Cash

- Should I Get a Life Insurance Loan for Cancer Treatment?

- How Do I Sell My Client’s Life Insurance Policy?

- Selling a Life Insurance Policy After a Terminal Diagnosis

- Can You Sell a Life Insurance Policy to Pay for Surgery?

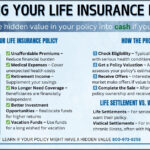

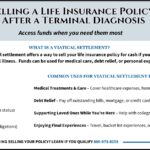

A viatical settlement is a financial arrangement in which a person sells their life insurance policy to a third party for a lump sum cash payment. This type of settlement is typically used by individuals who have a terminal illness and need cash to cover medical expenses or other bills.

Here’s an example of a viatical settlement to illustrate how it works:

Sarah, a 65-year-old individual, is diagnosed with a terminal illness and holds a life insurance policy with a face value of $500,000. Facing significant medical expenses and financial strain, Sarah decides to explore a viatical settlement as a way to alleviate her financial burdens.

She contacts a reputable viatical settlement company, which evaluates her policy based on her health condition and life expectancy. After careful assessment, the viatical settlement company offers Sarah a lump sum payment of $300,000, which is 60% of the policy’s face value.

Sarah accepts the offer, and the viatical settlement company becomes the new owner of her policy. They assume the responsibility of paying the remaining premiums until Sarah’s passing. Upon her death, the viatical settlement company receives the death benefit of $500,000.

Life expectancy plays a crucial role in viatical settlements. It refers to the estimated remaining lifespan of the insured. The longer the life expectancy, the longer it may take for the viatical settlement purchaser to receive the death benefit, impacting the potential return on investment.

In general, individuals with a shorter life expectancy are considered ideal candidates for viatical settlements. Individuals facing terminal or chronic illnesses are more likely to qualify for viatical settlements due to their diminished life expectancies, typically of 2-4 years or less.

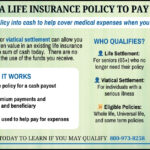

While life settlements and viatical settlements share similarities, they are not the same.

A life settlement involves the sale of a life insurance policy by a policyholder who no longer needs or can afford the coverage. Typically, life settlements cater to older policyholders without terminal or chronic illnesses. These individuals sell their policies to third-party investors or companies in exchange for a lump sum payment.

On the other hand, a viatical settlement is specifically designed for individuals facing terminal or chronic illnesses with significantly reduced life expectancies. Viatical settlements provide policyholders with the opportunity to sell their life insurance policies to viatical settlement companies or investors for an immediate lump sum payment. This financial transaction helps individuals access funds to cover medical expenses or enhance their quality of life during challenging times.

The key difference between life settlements and viatical settlements lies in the health condition of the policyholder. Life settlements are available to seniors without specific health conditions, while viatical settlements cater to individuals facing terminal or chronic illnesses.